Beauty, Entertainment, Food... TOP 40 rewards programs for customers in 2026

Read now

Insurance loyalty programs are essential to long-term growth, as McKinsey’s research shows that insurers who keep customers loyal outperform their peers dramatically in Total Shareholder Return – 20 percentage points higher in life insurance and 65 points higher in P&C from 2017 to 2022 (McKinsey & Company). Thus, as we say in Open Loyalty, when customers stay, profits rise.

Yet loyalty is harder to secure than ever. Churn is costing insurers $470 billion worldwide, and only 29% of customers feel satisfied with their provider (Accenture). Customers want more value between renewals: 88% expect personalized interactions, but 21% feel insurers don’t personalize at all. That unmet need is a major driver of switching.

Price alone is no longer what keeps customers. Bain & Company finds that in life insurance, a carrier’s reputation now influences retention more than cost. Especially as digital channels make comparison effortless (Bain & Company). EY’s latest outlook reinforces that in a world full of risk and uncertainty, long-term trust and relevance matter more than ever (EY).

The top insurance loyalty programs succeed because they offer ongoing value, reward loyalty, tailor every touchpoint, and connect engagement with lifetime value.

The next seven examples illustrate exactly how leading insurers are doing this and what you can adopt in your own strategy.

The following seven programs represent distinct strategic approaches to loyalty across European markets, from Nordic cooperative ownership and CEE multi-market platforms to German telematics simplicity and UK behavioral engagement. Each example demonstrates specific mechanics, customer workflows, and measurable outcomes that loyalty managers can adapt to their own market contexts and customer segments.

Tryg serves 3 million customers across Denmark, Norway, and Sweden, but its most powerful loyalty driver is the cooperative ownership model behind the brand. Its largest shareholder, TryghedsGruppen, is a member-owned cooperative that returns part of the insurer’s profit directly to policyholders.

Through the Annual Bonus Scheme, members receive 5 – 8% of premiums paid deposited straight to their bank accounts, effectively turning insurance into an ownership experience rather than a transactional purchase. The cooperative’s member-elected board determines bonus levels based on yearly financial results.

(In 2018 – edit.) Customer satisfaction reached record highs while customer retention was also at the highest level ever recorded. TryghedsGruppen paid out a member bonus for the fourth year running – now including the 380,000 Alka customers – meaning that 1.3 million customers (or approximately every fourth Dane) received a bonus equivalent to 8% of premiums paid in 2018 (source: Tryg Annual Report 2019)

This high-trust structure makes the program exceptionally transparent and sustainable. Bonuses have been paid every year since 2015, as confirmed in the Tryg Annual Report 2015. Awareness is also remarkably high, with 77% of members familiar with the scheme, driving strong word-of-mouth and reinforcing Tryg’s position as a consumer-centric insurer.

Key features:

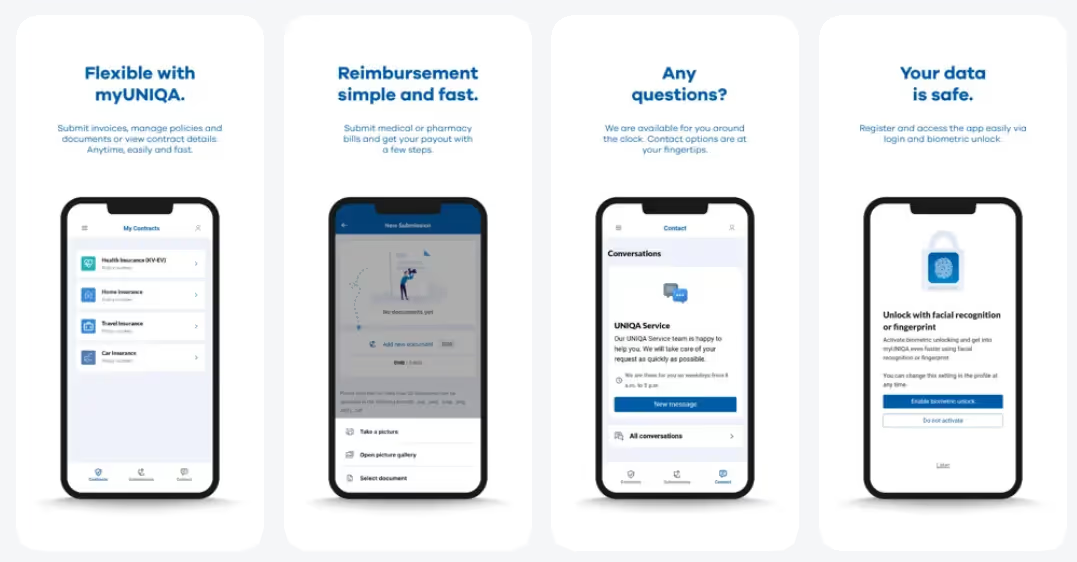

UNIQA, one of Central and Eastern Europe’s largest insurers with 16.7 million customers, launched myUNIQA plus in summer 2023 to modernize its loyalty strategy across multiple countries, according to the UNIQA CMD 2024 presentation

Built on a unified digital infrastructure spanning Austria and 14+ CEE markets, including Poland, the Czech Republic, Slovakia, Hungary, Romania, Bulgaria, Croatia, Serbia, Montenegro, Kosovo, Albania, Bosnia and Herzegovina, North Macedonia, and Ukraine, the program delivers a consistent experience powered by a single multi-language app, while adapting rewards and partner networks to each country’s consumer landscape.

The loyalty model centers on tier-based progression (Bronze, Silver, Gold) and a multi-dimensional earning system where customers accumulate points for policy purchases, app engagement, preventive health actions, digital submissions, and participation in promotional campaigns.

As members advance through tiers, they unlock increasingly valuable rewards, from basic online insurance discounts to premium partner benefits across travel, wellness, fitness, retail, and automotive services.

A key differentiator is myUNIQA plus’s localized reward catalogs, which ensure that benefits remain culturally and economically relevant in each region. Austrian customers access supermarket and outdoor-living partners; Polish customers receive discounts at convenience stores, fitness programs, electronics retailers, and diet-catering brands; while Czech customers benefit from health coverage add-ons and wellness networks.

Despite these differences, every market operates under a common loyalty architecture, supported by consistent omnichannel access, digital, call center, and agent-based.

The program is fully integrated into the myUNIQA app, which in 2023 served more than 630,000 users across markets (UNIQA Group Report 2023), allowing UNIQA to deploy the loyalty experience rapidly and at scale, without building separate platforms for each market.

Key features:

VHV, a German mutual insurer with 2.5 million auto insurance customers, drives loyalty through a radically transparent telematics model centered on real-time financial rewards.

Instead of complex gamification systems, VHV focuses on a single, clear value exchange: customers can earn up to 30% off their premium purely by demonstrating safe driving, with discounts calculated directly from live driving data.

This simplicity is reinforced by VHV’s assessment model – customers can qualify for their full discount within the first 25 driving hours, creating immediate visibility of value and eliminating the typical 60+ day evaluation phase used by competing telematics programs.

Continuous, real-time feedback shows customers how their behavior affects their discount, strengthening trust and encouraging safer driving habits. Behavioral psychology research confirms that instant feedback loops deliver significantly higher engagement than delayed annual evaluations.

This evidence-based structure makes the program highly transparent and so – effective. The combination of immediate savings, continuous insight, and low onboarding friction drives strong customer motivation and positions VHV as a consumer-first telematics provider.

Key features:

Allianz Partners, the travel insurance arm of Allianz Group, operates across 50+ countries with market-tailored loyalty initiatives rather than a single global program. While localized efforts such as Allianz Elevate in Sri Lanka emphasize lifestyle rewards and partner benefits, one of Allianz’s most powerful loyalty drivers is rooted not in perks but in claims innovation.

Launched in August 2018, the SmartBenefits feature, now available in the USA, Canada, Australia, and New Zealand, automates compensation for common travel disruptions, particularly flight delays. As detailed on the official Allianz website, customers receive automatic payouts of $100 per insured person per day for qualifying delays (typically 3–5 hours, depending on the plan terms), simply by registering their trip in advance.

By offering proactive claim payments on qualifying flight delays, our innovative SmartBenefits make it easier for customers to get paid quickly for their inconvenience. These enhancements to our travel protection products make traveling easier, more worry-free and enjoyable for our customers, stated Mike Nelson, Global CEO of Travel Insurance and Regional CEO for Americas.

This removes the traditional claims process entirely: no forms, no receipts, no friction. Allianz recognized that removing claims friction – travel insurance’s biggest customer pain point – creates stronger loyalty than conventional points-based programs.

Key features:

Aviva Journey, offered in the UK and Canada, is one of the most advanced smartphone-based telematics programs on the market. Developed with global telematics provider IMS, Journey combines two powerful loyalty levers: significant premium discounts and monthly gamified rewards (e.g., coffee vouchers).

Instead of relying solely on annual renewal discounts, Journey emphasizes real-time behavioral feedback, evaluating braking, acceleration, speed, cornering, and phone distraction using smartphone sensors, no hardware required.

Our IMS One App mobile telematics technology enables Aviva Canada to collect data insights as well as deliver meaningful engagement with their policyholders using the Aviva Journey app. The app collects extraordinarily rich data to help Aviva truly understand how customers are driving, and to link safe driving to financial rewards, said David Lukens, Senior Vice President for North America Sales for IMS.

After a 60-day or 400-mile observation period, drivers become eligible for performance-based premium reductions. Journey also includes crash detection and roadside support, making it a utility-driven app rather than just a loyalty tool.

Key features:

Aviva operates two structurally distinct telematics loyalty programs across its major markets – Aviva Journey in Canada and Aviva MyDrive in the UK – each designed to match regional driving culture, consumer expectations, and regulatory norms. Both programs are built on Aviva’s partnership with IMS (a global telematics provider), using smartphone-based data collection, but they deliver fundamentally different loyalty mechanics.

Aviva Journey, launched in June 2022, integrates real-time driving insights, upfront financial incentives, and gamified engagement features, encouraging consistent use throughout the policy term.

In contrast, Aviva MyDrive in the UK adopts a streamlined, discount-only model focused on simple price personalization. Instead of gamified rewards, MyDrive evaluates driving behavior through a short, compressed assessment period, providing early clarity on renewal pricing.

The emphasis is on fast evaluation and predictable premium adjustments, reflecting the UK market’s preference for transparency over ongoing in-app engagement.

Key features:

Insurance loyalty works differently than in retail, banking, or digital platforms. With few natural touchpoints and high-stakes moments, insurers must design programs that work with this reality, not against it.

Insurers interact with customers only a handful of times a year, often just at renewal or during a claim. These rare moments must support relationships that last decades. Because of this, loyalty mechanics built around constant engagement – points, badges, frequent prompts – tend to fall flat. Customers don’t want an ongoing relationship with their insurer; they want protection, fairness, and occasional, meaningful proof that their loyalty matters.

In a low-engagement category, programs that offer automatic rewards, cashback, profit-sharing, or easy-access discounts consistently achieve higher participation. They respect customer preferences and remove friction, especially for older or privacy-conscious segments.

Behavioral programs succeed only when participation directly improves customers’ lives. Real-time driving feedback, instant gym discounts, or meaningful wellness insights work because the value is immediate and personal; the insurance benefit becomes secondary.

In insurance, trust is earned at critical moments, especially claims. Eliminating paperwork, speeding compensation, or offering automated payouts creates lasting loyalty more effectively than points or tiers. When anxiety drops, retention rises.

Ultimately, insurance loyalty is built not through constant interaction but through credibility at the moments that matter. Programs that deliver clear, effortless value, whether through passive rewards, useful engagement, or frictionless claims, create trust that endures far longer than promotional incentives.

For loyalty managers, the goal is not to replicate retail-style engagement but to design mechanisms aligned with insurance psychology: reduce anxiety, increase fairness, and make benefits visible without demanding customer effort. When programs feel intuitive and respectful of how people naturally interact with insurance, participation rises organically.

The insurers that will win long-term loyalty are those that combine operational excellence with smart, customer-centric value delivery. By focusing on transparency, simplicity, and genuine utility, loyalty becomes a natural outcome of the overall experience, not an add-on customers must work to understand or maintain.

Programs that require minimal effort, such as automatic cashback, tenure-based rewards, or profit-sharing, tend to perform best across broad customer segments. They deliver value without demanding ongoing interaction, which fits naturally with how customers use insurance.

Engagement must deliver real utility, not artificial prompts. Real-time driving feedback, wellness insights, or preventive alerts encourage participation because they help customers improve safety or well-being immediately, values they care about beyond insurance discounts.

Tiers work well when customers understand the path to progress and when higher levels deliver meaningful benefits. They are most effective with digitally active segments who enjoy achievement-based motivation.

For older or privacy-conscious customers, simple, automatic rewards often perform better.

Claims are the single most decisive loyalty moment. A fast, transparent, low-friction claims experience often drives more retention than any points or perks.

Improving claims communication and automation typically yields the highest ROI of any loyalty initiative.

Yes, if the insurer has the digital maturity and actuarial justification to support them.

Real-time programs boost engagement and can reduce risk, but only succeed when feedback is immediate, intuitive, and personally beneficial. They should not be deployed purely for gamification.

Use a unified technology platform paired with local reward catalogs, ensuring operational efficiency while preserving cultural and economic relevance for each region. Central governance plus localized partner networks is the winning model.

API-first loyalty and gamification engine

Get a weekly dose of actionable tips on how to build and grow gamified successful loyalty programs!