Explore the top digital wallet software for enterprises, from payment and checkout wallets to loyalty-first platforms. Compare top solutions and use cases.

Digital wallets are becoming part of everyday customer behavior, with global adoption expected to pass 5.2 billion users by 2026. The real challenge starts when wallets need to work across mobile apps, websites, in-store systems, and existing loyalty stacks without breaking consistency.

For most enterprises, wallets quickly turn into more than a place to store payment methods. Customers expect points, cashback, vouchers, gift cards, and memberships to sit in one place, update instantly, and behave the same way wherever they interact. Tools built for a single purpose often fall short once programs grow beyond one channel or balance type.

Read on to see top enterprise digital wallet solutions, how they approach wallets and loyalty, and where each one fits depending on scale, use case, and technical setup.

Key takeaways

Clarify what role the wallet should play in your business. Enterprise wallets can support payments, rewards, engagement, or complex fund flows. The clearer the role, the easier it becomes to avoid tools that solve only part of the problem.

Treat consumer wallets as extensions, not foundations. Apple Wallet, Google Wallet, and similar tools work well as customer-facing layers, but they depend on another system to manage balances, rules, and logic behind the scenes.

Be cautious with infrastructure built for regulated money flows. Escrow- and compliance-heavy wallet platforms are well suited to marketplaces or public-sector use cases, but they often add complexity that loyalty-driven programs do not need.

Think twice before committing to custom development. Building a wallet from scratch offers control, but it also brings long delivery cycles, higher costs, and long-term responsibility for security, scaling, and change management.

Keep wallets and loyalty logic together. When balances, rewards, and rules live in separate systems, everyday changes become slower and harder to manage. Centralizing them simplifies operations and supports faster iteration.

Choose a platform that supports growth without re-architecture. Wallets that are natively connected to rewards, campaigns, and omnichannel logic allow programs to start focused and expand over time without stitching together additional tools.

What is digital wallet software?

Digital wallet software lets an organization create a virtual wallet where users can store and manage money, rewards, or credentials in one place. Instead of relying on physical cards, customers access everything through an app or web interface.

Data related to digital wallets speaks for itself. Approximately 53% of the global population used digital wallets to complete online transactions in 2024. Also, over 60% of online shoppers have used a digital wallet at least once.

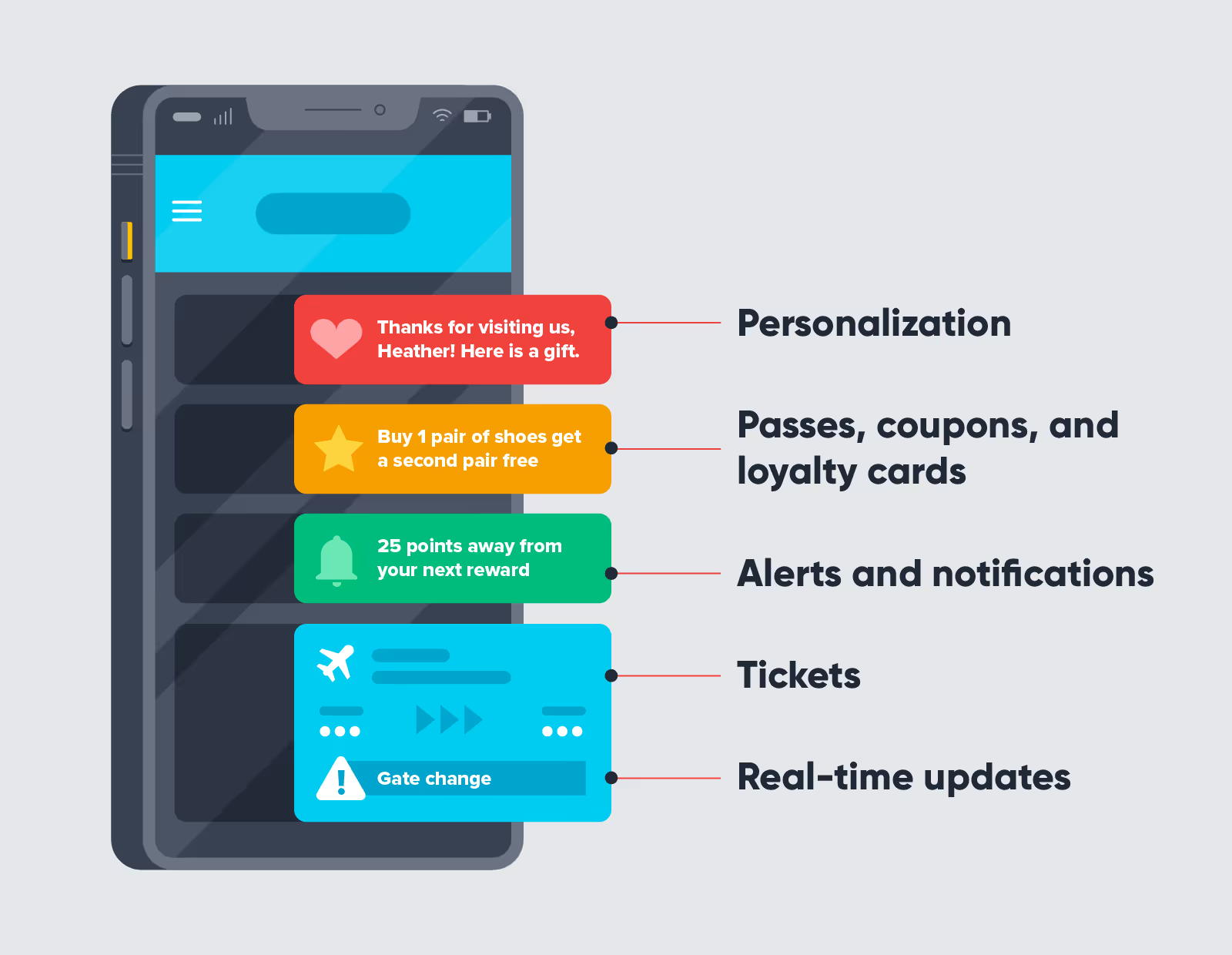

A digital wallet can store:

Payment cards

Loyalty points and cashback balances

Gift cards and vouchers

Membership or loyalty cards

Tickets, passes, or digital IDs

For enterprise teams, digital wallet system encompasses both the customer-facing experience and the underlying infrastructure. It includes the components necessary to issue wallets, manage balances, and maintain synchronization across systems and channels.

Enterprise wallet platforms usually provide:

Secure account storage with encryption

Multi-factor authentication methods such as biometrics or device-level security

APIs and integrations with payments, CRM, loyalty engines, and POS systems

Tools to manage wallet rules, balances, and transactions at scale

💡 Stay secure. Find out about loyalty fraud and how to prevent loyalty program abuse for your case.

At the enterprise level, wallets also need to hold up under real-world complexity. That means support for:

Large user volumes and high transaction frequency

Multiple currencies or point types

Real-time balance updates

Consistent behavior across mobile apps, web, and in-store environments

The difference between a basic wallet feature and an enterprise-ready platform usually shows up here: scale, control, and consistency across channels.

Why enterprises need digital wallet solutions (top 5 reasons)

Digital wallets rarely stay simple for long. Once an enterprise operates across channels, regions, and customer segments, wallets start touching payments, rewards, data, and everyday customer interactions.

The reasons below explain why many enterprises move beyond basic tools and invest in dedicated digital wallet solutions.

Reason

What it means for enterprise teams

Stronger loyalty engagement

A digital wallet keeps loyalty cards, rewards, and memberships visible on the customer's phone at all times. Points, cashback, and balances update automatically, encouraging repeat interaction without relying heavily on campaigns or reminders.

Higher purchase completion

Wallet-based payments reduce checkout friction, especially on mobile. Saved cards, balances, or vouchers help customers move from browsing to buying faster, supporting more consistent conversion rates across channels.

Loyalty-driven personalization

Wallet activity reveals how customers earn, spend, and ignore rewards. When connected with loyalty and CRM systems, this data enables more relevant offers, better timing, and segmentation based on real behavior.

Controlled security and governance

Enterprise wallets use encryption, tokenization, and device-level authentication to protect balances and payments. Audit logs, role-based access, and transaction tracking support internal controls and compliance.

Consistent omnichannel loyalty experiences

Wallet balances, vouchers, and membership status stay synchronized across apps, websites, and physical locations. Rewards earned in one channel are instantly available everywhere, reducing confusion and operational friction.

1. Boost customer engagement and loyalty

A digital wallet helps keep your brand present on the customer's phone, where attention already lives. When a loyalty card, points balance, or membership sits inside a wallet, it stays visible without relying on emails or reminders.

Enterprises often see higher participation with wallet-based loyalty compared to physical cards or email-driven programs because interaction feels effortless. Points and rewards update automatically, and customers can check their status in seconds.

Mobile wallets software also supports more relevant loyalty interactions. Enterprises commonly use them to deliver:

Birthday rewards directly to the wallet

Location-based offers when customers are near a store

Reminders about unused or expiring rewards

These moments feel timely and personal because they connect to real behavior. Compared to broad promotions, wallet-based rewards tend to feel more intentional and easier to act on.

Adoption does require upfront effort. Customers need a clear reason to add a wallet card or pass. Enterprises that see strong uptake usually focus on simple entry points, such as one-tap enrollment from email or SMS, paired with an immediate benefit like bonus points or an instant reward. Once customers start using the wallet, engagement often sustains itself.

Over time, an active wallet base supports repeat interaction, steadier loyalty participation, and stronger long-term attachment to the brand ecosystem.

2. Increase sales and conversions

Checkout friction shows up quickly in enterprise funnels. Every extra step increases the chance of drop-off, especially on mobile. Digital wallets reduce that friction by keeping payment details ready to use. Saved cards, stored balances, and one-tap flows remove the need to re-enter data, which makes completing a purchase feel straightforward.

Wallet adoption already reflects this behavior. Digital wallets are a major driver of this shift, increasing from 22% to 65% in eCommerce and from 3% to 45% in POS transactions. A large share of online transactions runs through digital wallets, and customers tend to stick with payment methods they recognize and trust.

When a preferred wallet is available, users move forward instead of hesitating. Wallets also reduce dead ends at checkout, since customers can switch between saved cards or use an existing balance without restarting the process.

Wallets also shorten the path from offer to purchase. Wallet-based payments shorten checkout time by up to 50%. One-tap or autofill flows remove multiple steps from the payment process, particularly on mobile. A reward or coupon delivered into a mobile wallet can link directly to a product page or checkout, with the discount applied automatically. That direct connection between incentive and payment functions supports faster decisions and higher redemption rates than traditional codes or emails.

What does this mean for you? The tighter loop between reward and transaction supports steadier conversion performance and higher revenue per active customer.

3. Harness data to personalize marketing

Another reason is that digital wallets generate a detailed stream of behavioral data. Each interaction, including payments, point earning, and reward redemption, adds context to how customers engage over time. When viewed together, these signals create a 360° picture of behavior, covering purchase frequency, average spend, preferred categories, and response to loyalty incentives.

Enterprise wallet platforms typically connect with loyalty and CRM systems, which allows wallet activity to map directly to individual customer profiles. That connection supports targeted communication based on observed patterns.

Customers who reduce activity can receive re-engagement offers tied to wallet usage. Those who frequently spend gift card balances can see product suggestions aligned with their past behavior. These interactions stay relevant because they reflect how customers already use the wallet.

Moreover, digital wallets can facilitate A/B testing of offers on a granular level. You can send different wallet promotions to segments and instantly see which drives more usage or new revenue streams, thanks to real-time analytics. The challenge for enterprises is handling this data securely and turning it into action. But those that do can move beyond one-size-fits-all campaigns to more intelligent loyalty strategies.

Ultimately, a wallet program helps you treat customers less like anonymous shoppers and more like known members with unique preferences.

4. Gain a competitive edge with modern experiences

Digital wallet support has become part of customer expectations across many industries. Seamless payments, app-based loyalty, and quick access to passes or rewards increasingly feel like the baseline.

Enterprises that roll out wallet-based experiences tend to stand out through smoother flows and more modern interactions, especially compared to brands still relying on physical cards or disconnected systems.

That difference shows up clearly in day-to-day use cases:

Travel brands storing boarding passes, lounge access, and frequent flyer points in one place

Retail brands appearing directly inside Apple Wallet or Google Wallet (passes, loyalty cards, payments)

Mobile-first experiences that reduce friction for repeat customers

These setups make choosing a brand easier, particularly for customers who already manage most of their activity on their phone (younger segments, frequent shoppers, commuters).

Wallets also influence customer behavior over time. When purchases, rewards, and balances live in one place, habits start to form. One-tap payments and visible loyalty balances reduce switching because customers already have history and progress tied to the wallet (points, status, stored value). Competitors offering similar products without that convenience often feel harder to use by comparison.

Adoption does come with trade-offs. Some customer segments need guidance during early rollout, and internal teams may need to adjust processes around wallets and loyalty data. Enterprises that work through that phase often see the payoff later, as wallet usage becomes part of routine behavior and supports long-term preference as digital-native audiences continue to grow.

Digital wallet software connects customer activity across channels into a shared layer. Stored balances, points, vouchers, or passes stay accessible whether customers shop online, use a mobile app, or visit a physical location (eCommerce, in-store, mobile). Points earned in one channel appear everywhere, and redemption follows the same rules across touchpoints.

For enterprise teams, a shared wallet layer simplifies day-to-day operations. One system acts as the reference point for balances and promotions, which reduces inconsistencies and manual reconciliation across tools and regions. Common logic, such as expiration dates or usage limits, behaves the same way everywhere (online, app, POS). That consistency leads to:

Fewer balance-related support cases

Less internal coordination between channel teams

Clearer ownership of loyalty and wallet rules

Wallet platforms also support broader business setups beyond traditional retail. Many enterprise wallets handle:

Stored-value accounts (prepaid balances, credits)

Escrow flows (holding funds until delivery conditions are met)

Multi-party payouts (marketplaces, platforms)

Financial institutions and telecom providers use wallets to combine payments, transfers, and loyalty cards in a single interface (often through QR codes or app-based access). Public sector programs rely on wallets to distribute funds with clear visibility and spending control. With the right platform, wallets support new services and partnerships without fragmenting the customer experience.

Best 10+ digital wallet software for enterprises

Looking to deploy a secure, scalable digital wallet for your enterprise? Discover a comparison of 10+ enterprise-ready digital wallet solutions, covering both white-label platforms you can build on and wallet ecosystems you can integrate with.

Each entry highlights where the platform fits best, what capabilities it offers, and why enterprise teams tend to choose it.

Solution

Primary focus

Wallet types supported

Loyalty and rewards depth

Payments and funds

Customization and control

Typical enterprise use case

Open Loyalty

Loyalty-first wallet platform

Points, cashback, gift balances, promo credits

Native (points, tiers, campaigns, gamification)

Through integrations

High (API-first, headless, white-label)

Enterprises running omnichannel loyalty programs with wallet-based rewards

SDK.finance

Fintech wallet infrastructure

Fiat, crypto, custom assets

External / basic

Native (banking-grade)

High (including source code option)

Banks, fintechs, regulated wallet products

Google Wallet

Consumer wallet ecosystem

Cards, passes, tickets

Pass-based only

Native (Google Pay)

Low (ecosystem rules)

Distributing loyalty cards and enabling Android payments

Apple Wallet

Consumer wallet ecosystem

Cards, passes, tickets

Pass-based only

Native (Apple Pay)

Low (ecosystem rules)

iOS payments and loyalty card distribution

PassKit

Wallet pass management

Loyalty cards, coupons, tickets

Pass-level only

None

Medium (pass design and logic)

Wallet-based loyalty without building wallet infrastructure

ClassWallet

Controlled spend wallet

Program funds

None

Native (restricted spending)

Medium

Education, public sector, grants, benefits programs

MetaMask (Institutional)

Crypto and Web3 wallet

Crypto assets, NFTs

None

Blockchain-based

Medium

Institutions operating in DeFi and Web3

Link (Stripe Link)

Accelerated checkout wallet

Payment credentials

None

Native (Stripe network)

Low

eCommerce checkout optimization

Limeup (Custom build)

Bespoke wallet development

Fully custom

Fully custom

Fully custom

Very high (code ownership)

Enterprises building a proprietary wallet from scratch

SoftwareGroup

Banking and telco wallet platform

Stored value, bank-linked

Basic

Native (banking-grade)

High

National wallets, telco wallets, financial inclusion initiatives

Mangopay

Marketplace payment wallet

Escrow wallets, balances

None

Native (escrow, payouts)

Medium

Marketplaces, platforms, crowdfunding

1. Open Loyalty

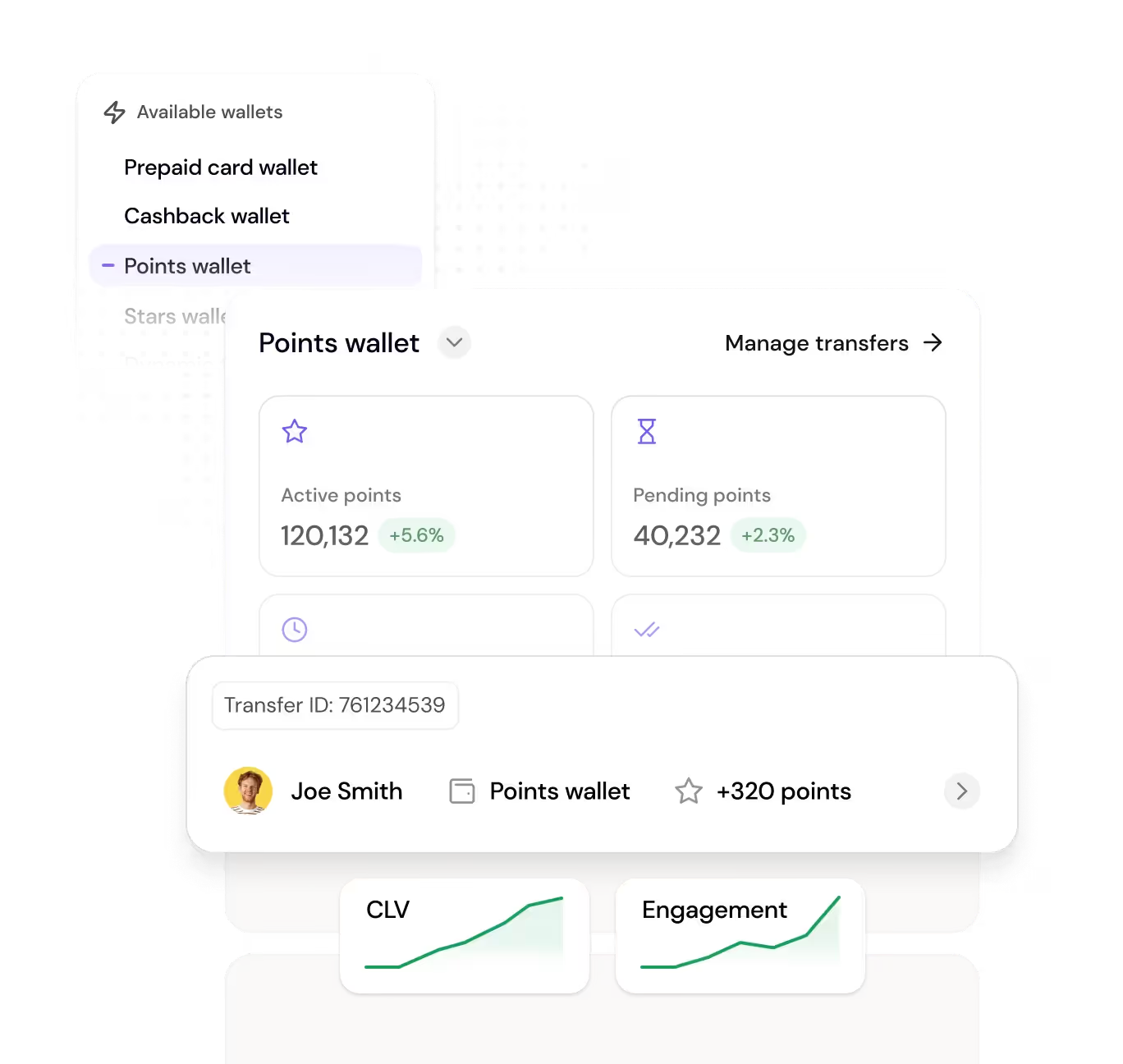

Open Loyalty is an API-first loyalty and wallet engine built for enterprises that need full control over how reward-based value is issued, stored, and used. Rather than offering a fixed consumer wallet or handling regulated money, it provides the infrastructure to create custom digital wallets for points, cashback credits, gift balances, and other loyalty-driven value types, all managed within a single platform.

Enterprises use Open Loyalty to launch branded wallet experiences where rewards and incentives are tightly connected to customer activity. Earn, store, and spend value inside one ecosystem, with clear rules, real-time updates, and full visibility across channels.

Multiple wallet types. Open Loyalty supports several wallet models out of the box, including points ledgers, cashback wallets, prepaid balances, and gift card wallets. Enterprises can run multiple wallets in parallel within one program (for example, separating promotional points from gift balances) without building separate systems.

Flexible currency and balance rules. Each wallet currency comes with configurable logic. Teams define expiration windows, activation delays, conversion rates, and usage limits per currency or per campaign. Promotional points, long-term points, or region-specific balances can coexist and behave differently while remaining fully automated.

Real-time balance updates and events. Wallet balances update instantly when customers earn or spend value. Transaction events can trigger notifications through APIs or webhooks, allowing enterprises to surface updates inside their apps or communication channels (earn confirmations, redemptions, balance changes) across mobile, desktop, totems, and other interfaces.

Headless, integration-ready architecture. Open Loyalty runs fully headless. All wallet operations are available through APIs and webhooks, which makes it easy to connect eCommerce platforms, POS systems, mobile apps, CRM tools, or internal services. Wallet data stays consistent regardless of where the customer interacts.

Enterprise-grade security and scale. The platform meets enterprise security expectations with ISO 27001 certification, GDPR alignment, role-based access, and audit logs. It supports high traffic volumes and large member bases, with cloud and on-premise deployment options depending on organizational needs.

Built for loyalty-driven growth, not payment infrastructure. Open Loyalty approaches wallets as part of a broader loyalty strategy. Points, rewards, tiers, referrals, and gamified mechanics are native to the platform. Wallets act as the operational layer where loyalty value moves, rather than an add-on bolted onto payment flows.

Composable instead of all-in-one. Enterprises with mature tech stacks often don’t want another monolith. Open Loyalty fits into existing architectures, allowing teams to use only what they need and connect loyalty logic to their own apps, data layers, and customer journeys.

Designed for behavior, not just transactions. Beyond purchases, wallets can reward actions like app usage, referrals, reviews, challenges, or milestones. This supports gamified programs that focus on repeat behavior and long-term engagement rather than short-term discounting.

Operational agility without heavy development. Many wallet and reward rules can be configured through the admin interface, allowing marketing and loyalty teams to iterate on campaigns, balances, and mechanics without constant developer involvement.

A practical alternative to building from scratch. For enterprises weighing custom development, Open Loyalty provides a proven foundation for wallet and loyalty logic while leaving front-end experiences and differentiation in-house. This reduces delivery risk and long-term maintenance burden without limiting flexibility.

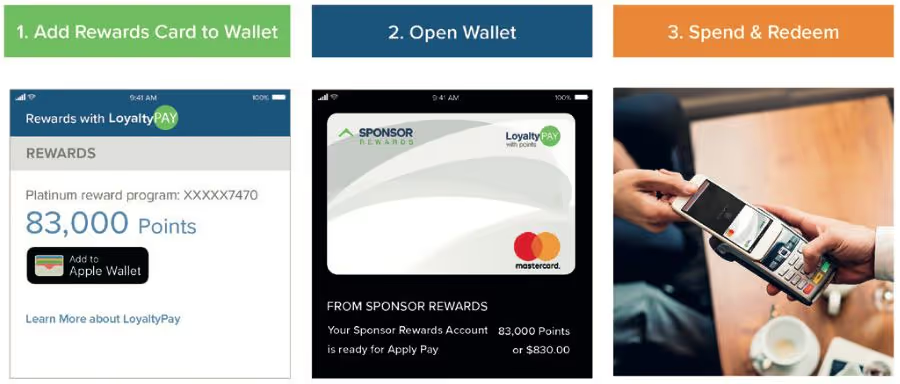

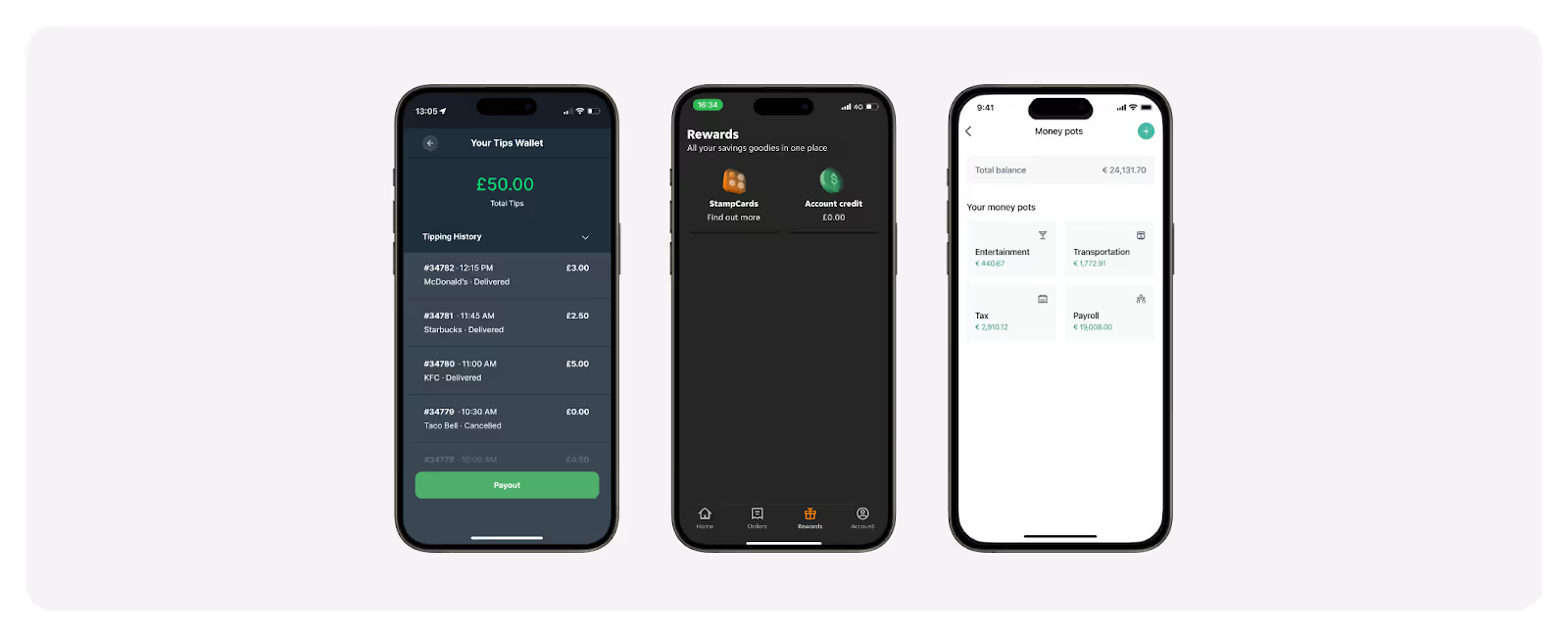

Digital software wallet by Open Loyalty. Source: https://www.openloyalty.io/product/digital-wallet-software

Open Loyalty clients appreciate the loyalty platform and its retail capabilities, saying:

"The software has been easy to use and understand. The API documentation is kept up to date and is easy to consume. The team at Open Loyalty is great, they consistently provide good service and are willing to help if required."

"The application is very responsive at all times and has been designed for scalability, which we've never had the need to do since the default configuration is more than enough for our customers' user base. We've implemented this solution with several clients, and it's been a really quick and easy solution that has kept our customers happy."

"It was a successful project with great support from the supplier. In a very short time, our client was able to launch a loyalty program with personalized strategies and a portal for their clients."

👉 Read more opinions on Open Loyalty on G2 or Capterra.

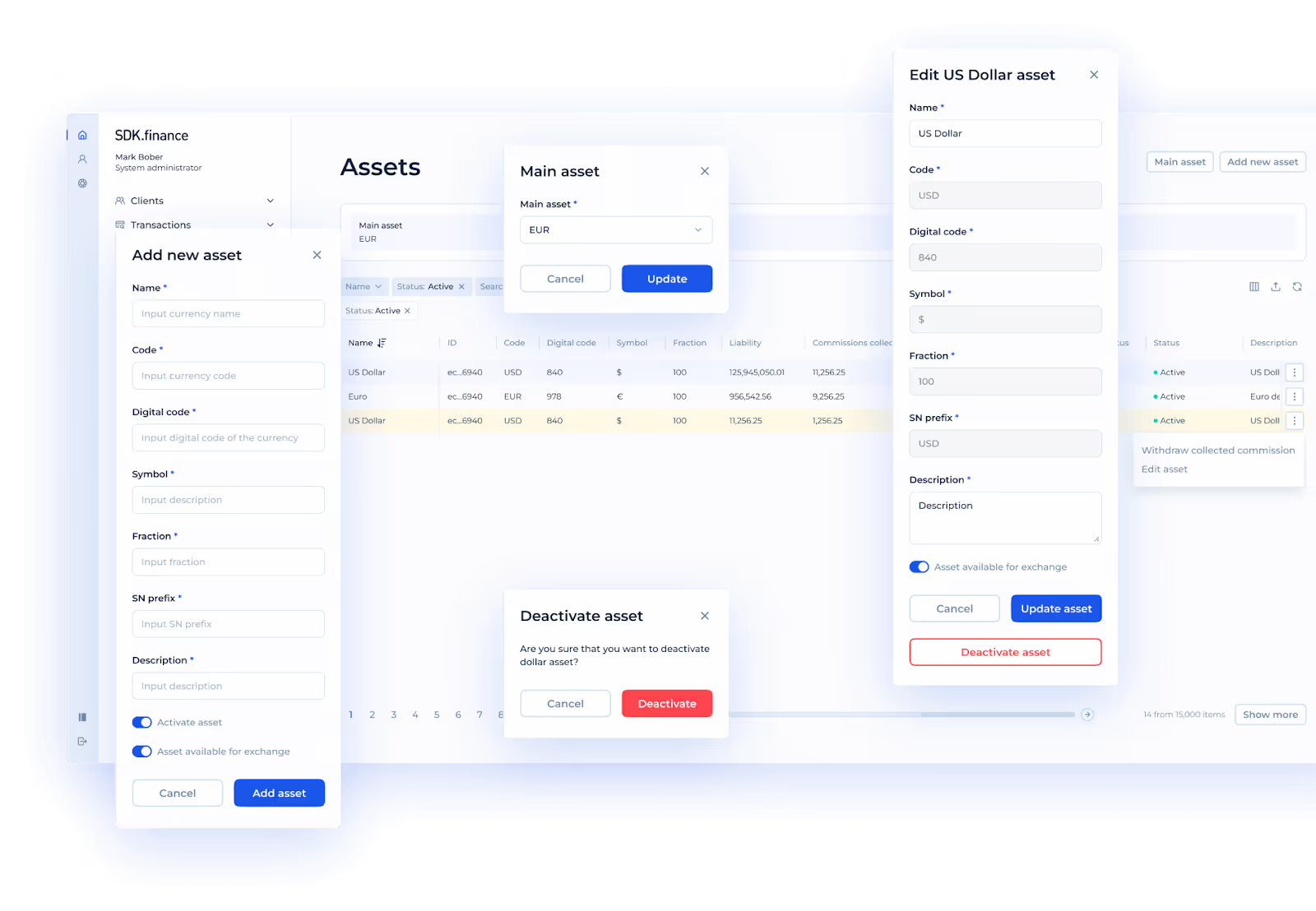

SDK.finance is a white-label digital wallet platform positioned mainly as a fintech infrastructure toolkit. It provides backend components for e-wallets, neobank applications, payment systems, and account-based products.

The solution is commonly used by financial services organizations and fintech teams that need to launch regulated wallet products covering bank accounts, payments, and ledger management.

Digital wallet features for enterprises

Accounts for multiple currencies and assets. The platform supports wallets for fiat currencies, cryptocurrencies, and custom assets such as loyalty points or miles. Each asset type is tracked through an internal ledger that records balances and transactions.

Payments and money transfers. Built-in modules support bank transfers (including IBAN and SWIFT), peer-to-peer payments, bill payments, and digital currency exchange. Wallet users can top up balances, transfer funds, or pay utility bills within the same system, which aligns closely with banking and payment-centric use cases.

Card issuing and payment acceptance. Integrations with external card providers allow virtual or physical cards to be linked to wallet balances. The solution also connects to payment gateways to accept card payments into the wallet, a common requirement in financial or telecom-oriented wallet programs.

Prebuilt UI and administrative tools. A white-label mobile app interface and an admin back office are included. The admin panel supports onboarding flows, transaction monitoring, rule configuration, and customer support workflows. Enterprises can use the provided UI as a base or customize it further.

Compliance-oriented security features. The platform includes KYC and AML tooling through third-party integrations, along with authentication controls, audit logs, and permission management. These capabilities address regulatory requirements typically found in financial services environments.

Why enterprises choose it

Broad fintech coverage in one system. Enterprises select this solution when they want payments, accounts, cards, and transfers handled within a single platform. It often replaces the need to integrate multiple financial systems, which suits banking-style or super-app projects more than loyalty-driven programs.

Source code licensing option. An option to license the source code is available for organizations that want full internal control over the platform. Such an approach appeals to teams aiming to avoid vendor dependency, though it also increases internal ownership and maintenance effort. A hosted model is also available.

Used in high-volume financial scenarios. The platform has been deployed in national wallet initiatives and benefit distribution programs. These examples show its ability to operate at scale, particularly in transaction-heavy and regulated environments.

Support for multiple asset types. Wallets can handle fiat currency alongside digital assets such as crypto or tokenized rewards. The described flexibility suits enterprises exploring financial or asset-management extensions rather than focused loyalty ecosystems.

API-based extensibility. The architecture exposes modular APIs that allow teams to extend or integrate individual components, such as onboarding or payment flows. Development-heavy organizations often use this flexibility to adapt the platform to specific regulatory or operational needs.

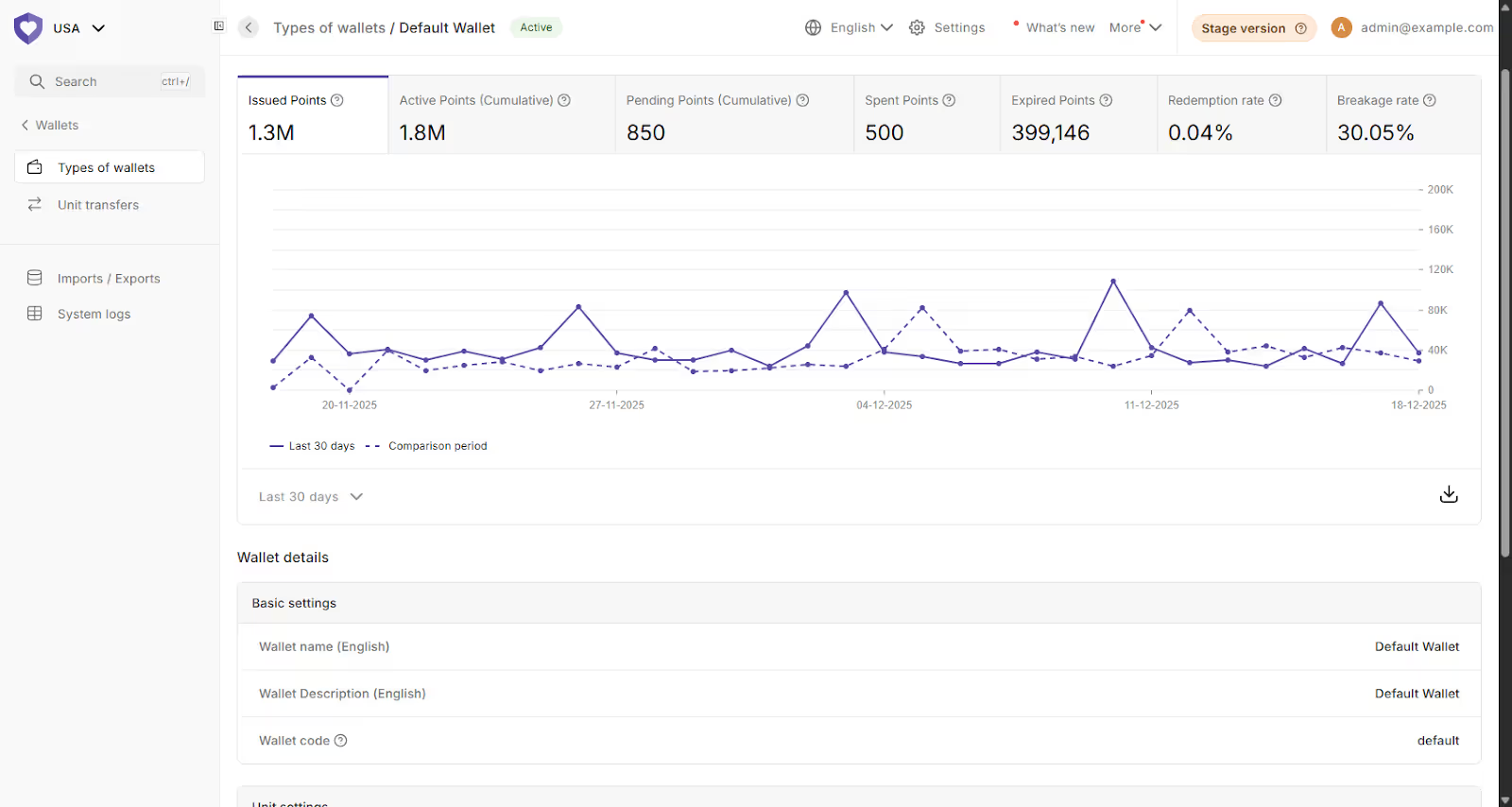

SDK.finance dashboard.

3. Google Wallet (Google Pay)

Google Wallet is a consumer wallet ecosystem available on Android devices and the web. Rather than a platform enterprises deploy or run themselves, it acts as an integration layer that allows customers to store payment cards, loyalty cards, passes, and tickets on their devices.

For enterprise teams, supporting this wallet usually means making their cards or payments compatible with it, treating it as a distribution channel within a broader wallet or loyalty strategy.

Digital wallet features for enterprises

Loyalty, gift, and membership passes. Enterprises can create digital loyalty cards, membership cards, gift cards, coupons, and event tickets that customers save to their wallet. Using available APIs, businesses define pass structure, branding, and data fields such as points balance or membership level. Once saved, passes can update dynamically, for example when a points balance changes after a transaction.

Payment integration through Google Pay. Credit and debit cards stored in the wallet can be used for contactless NFC payments in physical locations and for online checkout flows. Enterprises can add this payment method to apps or websites to support faster checkout using already-saved cards.

Cross-device and cloud-based access. Wallet passes are linked to a user's account and stored in the cloud, which allows them to sync across supported Android devices. Passes can be added through websites, emails, or QR codes, which means enterprises can distribute cards without requiring users to install a dedicated mobile app.

Engagement and update mechanisms. The wallet supports notifications and location-based alerts associated with saved passes. Enterprises can trigger reminders when customers are near a store or update pass content when offers expire or change.

Security handled at the platform level. Payments rely on tokenization and device-level authentication such as screen lock or biometrics. Passes are signed and protected from user modification, while sensitive data is stored using device security features.

Why enterprises choose it

Large existing adoption among consumers. Many customers already use this wallet for payments and passes on Android devices. Supporting it lowers the effort required for customers to save cards or use mobile payments, as it fits into existing behavior.

Faster checkout for Android traffic. Wallet-based payments reduce the number of steps required during mobile checkout. Saved cards and one-tap flows limit manual entry, which often leads to fewer abandoned carts on Android devices.

Pass distribution without a proprietary app. Enterprises can issue loyalty cards, coupons, or tickets through links or QR codes without maintaining their own mobile application.

Integration with surrounding Google services. Wallet passes can surface through related services such as email confirmations or device-level reminders. For example, boarding passes or loyalty cards may appear automatically when relevant.

Platform-managed evolution. New pass types and capabilities are added over time at the ecosystem level.

Google Wallet (Google Pay) dashboard.

4. Apple Wallet (Apple Pay)

Apple Wallet is a consumer digital wallet available on iOS devices. It allows users to store payment cards, loyalty cards, tickets, and other passes directly on their iPhone or Apple Watch. Alongside it, Apple Pay provides contactless and in-app payment functionality.

For enterprises with a large iPhone user base, it typically acts as a delivery channel for digital cards and a payment option at checkout. It complements internal wallet or loyalty infrastructure rather than replacing it.

Digital wallet features for enterprises

Passes for loyalty, coupons, and tickets. Enterprises can issue digital passes for loyalty cards, gift cards, coupons, event tickets, and boarding passes. Passes are created using Apple's PassKit framework and distributed through apps, emails, or links.

Payments through Apple Pay. Credit and debit cards added to the wallet can be used for contactless payments in physical locations and for one-tap payments in apps or on websites. Transactions rely on device-specific tokens and require biometric or device authentication.

Hardware-backed security model. Payment card data is stored in the device's Secure Element and isn't exposed to apps or servers. Biometric authentication through Touch ID or Face ID is required for transactions. Loyalty and other passes are signed with certificates to prevent tampering, even though they do not store sensitive payment data.

Context-aware pass presentation. Passes can surface automatically based on time or location. Examples include boarding passes appearing near flight time or event tickets showing on the lock screen at a venue. Loyalty cards can be configured to appear when a customer is near a store, reducing the need for manual searching.

Integration with apps and backend systems. Passes are typically integrated using PassKit APIs from mobile apps or backend services. NFC capabilities are also available for certain pass types. Payment integration follows Apple's defined APIs or supported gateway flows.

Why enterprises choose it

Access to a high-spend customer segment. Usage of this wallet and payment method is common among iPhone users, particularly in markets with higher mobile commerce adoption.

Familiar user experience and platform trust. Wallet functionality is built into every iPhone, and payment flows rely on biometric confirmation. Many customers prefer saving cards or passes in a system they already use, rather than installing additional apps..

Reduced exposure to payment data. Tokenized payments and device-level authentication limit the handling of raw card data on the enterprise side. Mentioned setup can reduce fraud exposure and simplify internal compliance processes compared to traditional card handling.

Support for contactless behavior. Contactless payments continue to grow across regions. Supporting this wallet allows enterprises to meet customer preferences for tap-based payments in-store and faster checkout online, particularly on mobile devices.

Distribution of digital loyalty cards without an app dependency. Loyalty cards and passes can be delivered through email or web links, even without a dedicated iOS app. Enterprises use this approach to replace physical cards or reduce reliance on full app installations, while still keeping their brand visible on the customer's device.

Apple Wallet (Apple Pay) dashboard.

5. PassKit

PassKit's a platform focused on creating and managing mobile wallet passes for Apple Wallet and Google Wallet. It does not function as a standalone wallet or loyalty engine, but rather as an enablement layer that helps enterprises issue, update, and distribute digital passes.

From an enterprise perspective, it acts as tooling around pass creation, delivery, and lifecycle management, sitting alongside existing CRM, loyalty, or backend systems.

Digital wallet features for enterprises

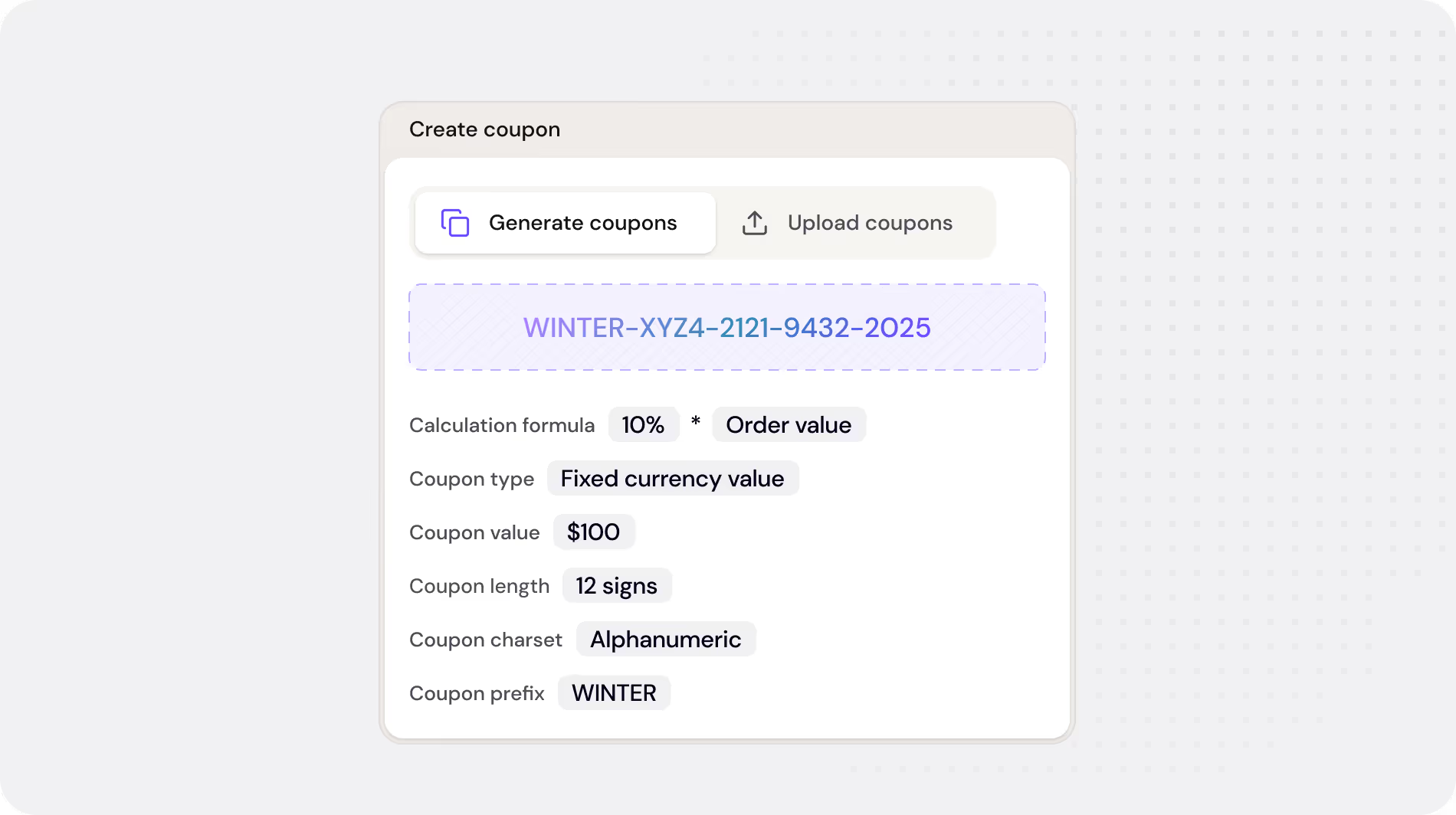

Universal pass creation. The platform supports creation of passes for loyalty cards, membership cards, coupons, gift cards, event tickets, and boarding passes. Enterprises can design passes using templates or a no-code editor, add branding, custom fields, and barcodes or QR codes, and generate formats compatible with both major wallet ecosystems.

Dynamic updates and real-time pass changes. Issued passes can update after distribution. For example, a loyalty pass can reflect a new points balance or status change without requiring the customer to re-download it. Notifications can be triggered through the wallet framework to inform users about updates or new rewards.

APIs and system integrations. APIs, webhooks, and automation connectors allow wallet events to link with CRM, POS, or marketing systems. Enterprises commonly use these integrations to issue passes when a customer joins a program or to update pass content based on changes in internal systems.

Scalable infrastructure for large deployments. The platform is designed to support high pass volumes and global distribution. Security certifications and uptime commitments support enterprise use cases, and dedicated environments are available for organizations with higher compliance or volume requirements.

Wallet campaigns without a mobile app. Passes can be distributed through hosted landing pages, links, or QR codes. Such an option allows enterprises to run wallet-based loyalty or coupon campaigns without requiring customers to install an app or create an account, which lowers participation barriers for short-term or broad-reach initiatives.

Why enterprises choose it

Shorter rollout timelines. Enterprises often select this solution to digitize loyalty cards or promotions without a full mobile development process. Templates and managed infrastructure allow programs to launch faster compared to building custom wallet integrations internally.

Engagement-focused pass features. Built-in support for notifications, location triggers, and dynamic updates allows passes to stay visible and relevant after being saved.

Single tooling for iOS and Android wallets. One setup can be used to deploy passes to both major wallet ecosystems. It simplifies operational overhead and avoids maintaining separate implementations for different device platforms.

Established experience with wallet ecosystems. The vendor has long-standing experience working with wallet standards and provides documentation and guidance around pass design and delivery. Enterprises often rely on this expertise when launching wallet-based campaigns for the first time.

Security and operational reliability. Enterprise customers reference security certifications, global infrastructure, and proven uptime as reasons for choosing the platform.

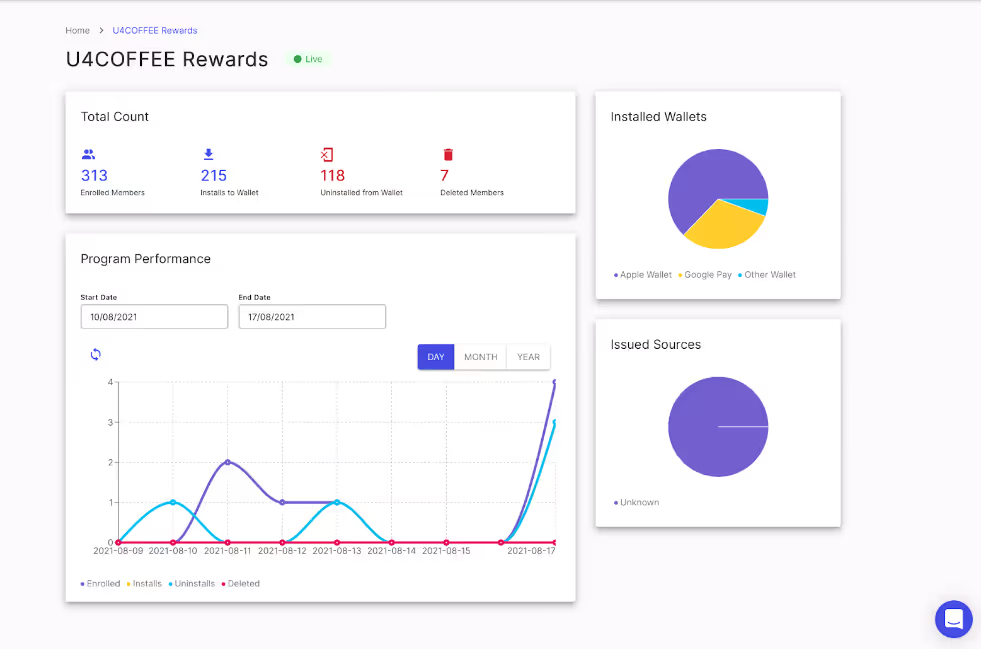

PassKit dashboard.

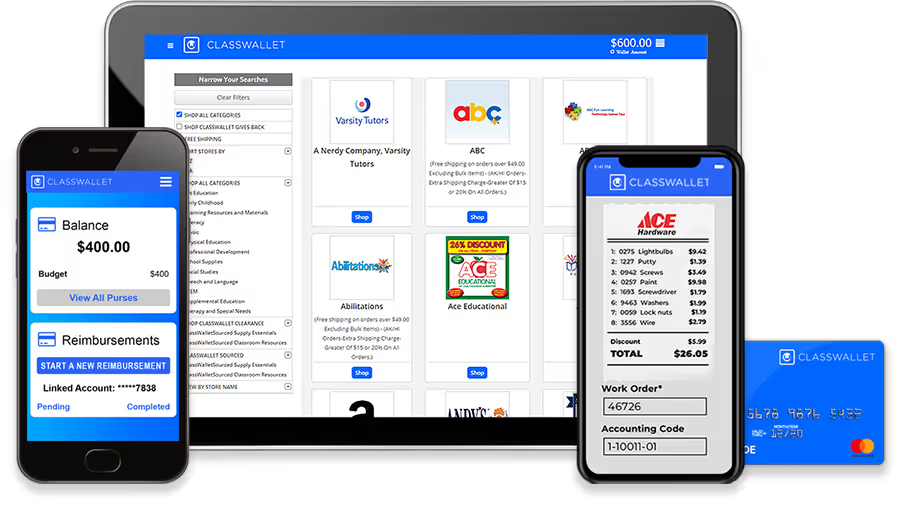

6. ClassWallet

ClassWallet is a digital wallet platform designed specifically for education and public sector organizations. It focuses on controlled fund distribution for use cases such as school budgets, grants, scholarships, and public benefit programs. Rather than operating as a general-purpose wallet or loyalty system, it functions as a spend management wallet with built-in oversight and compliance controls.

The platform is commonly used by government agencies and school districts to allocate funds to individuals, such as teachers or families, who can then spend those funds within predefined rules. Its core emphasis sits around auditability, transparency, and administrative control in regulated funding environments.

Digital wallet features for enterprises

Program-specific wallets for recipients. Organizations can create individual wallets for each recipient, such as teachers receiving classroom budgets or families receiving scholarship funds. Funds are loaded digitally and tagged for specific purposes.

Marketplace and vendor controls. The platform includes a marketplace of pre-approved vendors, such as office supply or educational material providers. Wallet funds can be spent only within allowed vendors or categories. Seamless integration with procurement systems and support for virtual cards further reinforce spending restrictions tied to program rules.

Transaction tracking and reporting. Every wallet transaction is logged with full visibility into amount, recipient, vendor, timing, and category. Administrators receive audit-ready reports that support compliance reviews.

Approval workflows and role-based access. The system supports approval flows for reimbursements or purchases. Different roles, such as teachers, administrators, or auditors, see only the data relevant to them.

Security and compliance controls. The platform is designed to meet government security standards and undergoes regular audits. Fund movement is fully traceable, and data is stored with controls suited for public sector requirements.

Why enterprises (and agencies) choose it

Purpose-built for public fund distribution. Organizations in education and the public sector adopt this solution because it addresses a very specific problem: managing how public funds are spent. Manual grant or budget processes are often slow and error-prone.

Reduced administrative workload. Digitizing fund distribution and reimbursement reduces time spent on reconciliation and reporting. Agencies report fewer manual processes and faster turnaround for fund access. Staff can focus more on program outcomes instead of administrative tasks.

Built-in audit readiness. Compliance requirements are enforced through system rules rather than after-the-fact reviews. Auditors can access reports directly or receive structured exports on demand.

Accessible for non-technical users. The interface is designed for teachers, parents, and officials who may not be familiar with financial software. Spending through approved vendors or submitting receipts follows guided flows, which supports adoption across diverse user groups.

Established adoption in regulated programs. The platform has been used to distribute large volumes of public funds across multiple state-level programs. Its presence across education departments and scholarship initiatives provides reassurance for organizations evaluating similar fund distribution use cases.

ClassWallet dashboard.

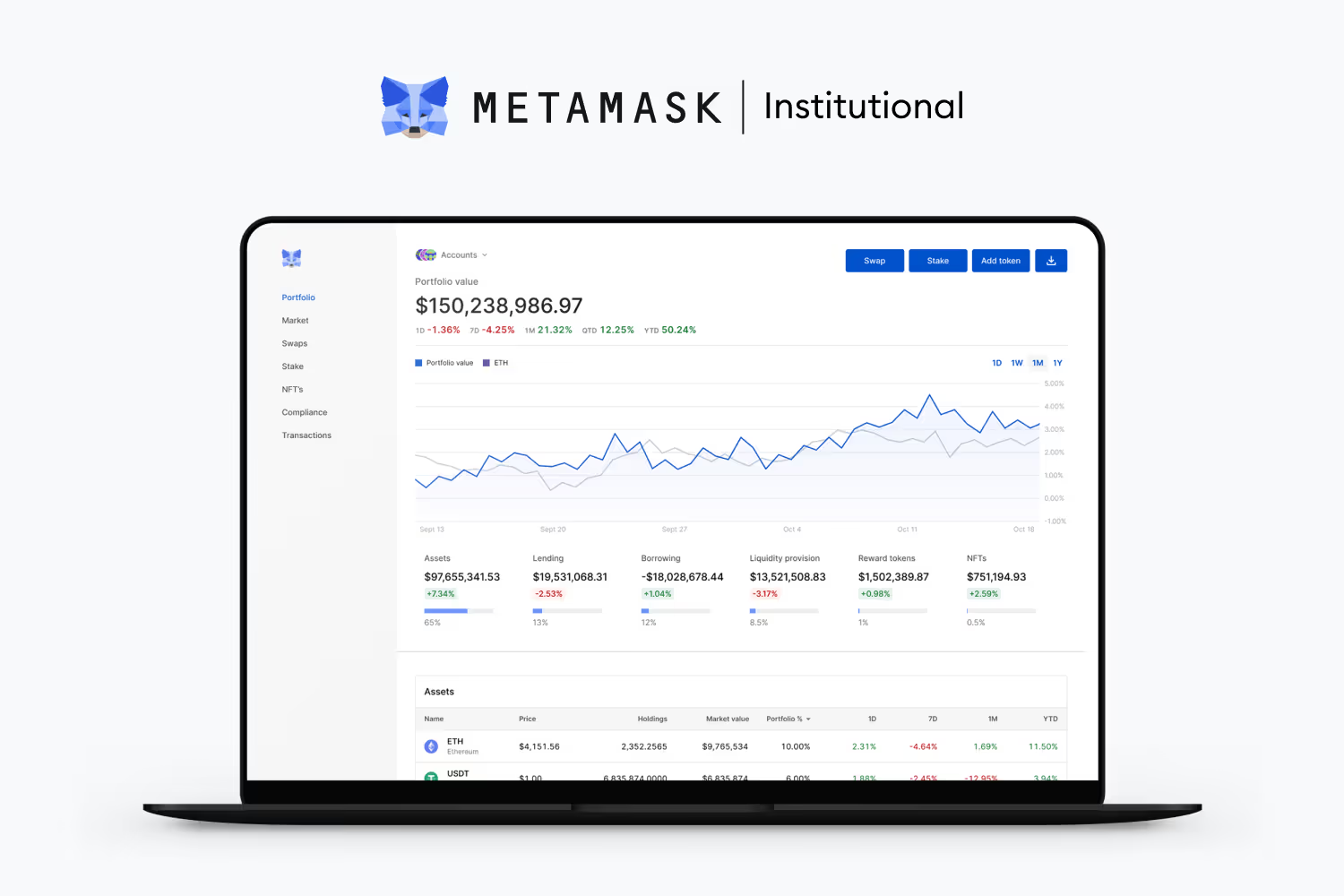

7. MetaMask (Institutional)

MetaMask is a cryptocurrency wallet primarily used for interacting with Ethereum and other blockchain networks. Originally built as a consumer browser wallet, it also offers an institutional version aimed at organizations such as crypto funds, financial institutions, and enterprises operating in Web3 environments.

For enterprises exploring blockchain use cases, the institutional version adds organizational controls, custody integrations, and compliance tooling on top of the core wallet functionality.

Digital wallet features for enterprises

Multi-chain crypto asset support. The wallet can store and manage cryptocurrencies and tokens, particularly Ethereum-based assets such as ERC-20 tokens and ERC-721 NFTs, with additional chains supported through compatibility layers or add-ons.

DApp integration and Web3 connectivity. A core capability is acting as a gateway to decentralized applications. Web3 functionality is injected into the browser so institutional users can connect to DeFi protocols, NFT marketplaces, and other blockchain applications with minimal setup.

Institutional controls and compliance layer. The institutional offering adds features that standard consumer wallets do not cover well in organizational settings, including multi-user access with roles, transaction approval workflows, and reporting. It can integrate with custody providers so that when a team member initiates a transaction, custodian policies apply (for example, multi-signature approvals, risk checks, or other controls).

Custody integrations and enterprise security options. Enterprises can configure setups that avoid a single seed phrase model. Custody integrations allow private keys to remain under custody provider control, while the wallet acts as a front-end for initiating activity. MPC (multi-party computation) and multi-signature configurations can be used through integrated custodians or security providers, reducing single points of failure compared to unmanaged personal wallets.

Portfolio views and analytics. The institutional tooling provides dashboards that show holdings across accounts and protocols. Depending on configuration, this can include portfolio visibility, performance tracking, exposure views by asset, and other reporting used by funds or financial institutions. These core features matter mainly when organizations need internal reporting or client-facing transparency around crypto and financial operations.

Why enterprises choose it

Access to Web3 ecosystems that already support it. Many decentralized applications are built to connect through this wallet standard. Enterprises that need to interact with DeFi protocols, decentralized exchanges, NFT tooling, or other Web3 services often use it as a connection layer, rather than building custom integrations for each application.

Familiar interface with an enterprise overlay. Teams that already used the consumer wallet tend to find the interface recognizable, which reduces training requirements. Organizational controls sit behind the scenes (approvals, roles, reporting), allowing day-to-day users such as traders or portfolio managers to operate through a known workflow while compliance and security controls remain enforced.

Compatibility with existing custody requirements. Enterprises often work with custody providers for regulatory, risk, or governance reasons. The institutional version integrates with multiple custodians and enterprise custody tools, allowing assets to stay with a chosen custody partner while still using the wallet interface to interact with Web3 applications.

Operational controls for institutional activity. Approval workflows, audit logs, role-based permissions, and policy controls help reduce risks such as unauthorized transactions or process gaps. Some setups also allow address allowlists, spending limits, and multi-step approvals, which are common requirements for institutional crypto activity.

Alignment with a widely used wallet standard. Enterprises sometimes choose it because it maps to a broadly adopted Web3 connection method and tends to stay compatible with ongoing ecosystem changes.

MetaMask (Institutional) dashboard.

8. Link (Stripe Link)

Link is a digital wallet and accelerated checkout solution built by Stripe. It's designed to let consumers save their payment and shipping details once and reuse them across a large network of participating businesses for faster checkout. It does not operate as a standalone consumer app or a branded wallet experience, but instead lives directly inside checkout flows powered by Stripe.

From an enterprise perspective, supporting it means allowing customers to reuse previously saved credentials to complete purchases more quickly. It can be applied even to first-time buyers on a given site, as long as they have used the wallet elsewhere within the network. The solution focuses specifically on reducing checkout friction rather than managing balances, loyalty, or stored value.

Digital wallet features for enterprises

One-click checkout with saved customer details. When a user opts in on a Stripe-powered site, their payment card information, email address, phone number, and shipping addresses are securely saved. On subsequent checkouts at any participating business, users can authenticate with a one-time code and instantly populate all required fields.

Shared payment credentials across merchants. Saved details are usable across a large network of Stripe-enabled businesses. For enterprises, this means customers may arrive at checkout already able to complete a purchase with minimal interaction, even if they have never shopped with that brand before.

Multi-device and browser availability. Saved credentials are accessible across devices and browsers. Users can complete purchases on mobile or desktop with the same wallet data, and can store multiple payment methods and shipping addresses.

Subscription visibility and payment management. Users who access their wallet account can view and manage subscriptions associated with saved payment credentials. For enterprises offering recurring billing, this indirectly supports better continuity, as customers have a centralized place to update card details used across services.

Security and fraud protection through Stripe. Payment data is encrypted and stored within Stripe's PCI Level 1 compliant infrastructure. Each new device or checkout session requires one-time passcode verification to confirm identity.

Why enterprises choose it

Reduced checkout abandonment, especially on mobile. Long checkout forms are a common cause of drop-off, particularly on mobile devices. Enterprises adopt this solution to shorten the time between intent and purchase, which can improve completion rates for impulse and repeat purchases.

Network effects across a large merchant base. Millions of shoppers have already saved their information through previous purchases within the Stripe ecosystem.

Low overhead for Stripe-based implementations. For organizations already using Stripe, enabling this functionality requires limited additional integration. Checkout flows remain embedded within the merchant's site, avoiding redirects and preserving branding and UX control.

Externalized handling of sensitive data. Enterprises do not store or process raw card details. Payment data handling, end-to-end encryption, and fraud prevention are managed by Stripe, which reduces internal compliance scope and operational burden.

Improved stability for subscription revenue. Centralized management of payment credentials means users are more likely to update card details proactively. When payment information is updated once and applied across subscriptions, enterprises may see fewer failed charges caused by expired or replaced cards.

Link (Stripe Link) dashboard.

9. Limeup (Custom Wallet Development)

Limeup is a software development company that builds custom fintech and digital wallet solutions for enterprises. It typically appears in conversations when organizations decide that ready-made platforms do not fit their requirements and a bespoke wallet application is needed instead.

Enterprises engage this type of vendor when the wallet itself is treated as a custom product rather than a configurable platform. The outcome depends heavily on the scope, budget, and internal capabilities of the organization commissioning the build.

Digital wallet features for enterprises

Tailored functionality based on business model. Wallet features are defined project by project. Implementations may include loyalty points, gaming tokens, multi-currency support, or specialized payment logic depending on the use case. Functionality is built to specification, which can include offline payments, multi-signature accounts, or integration with connected devices such as vehicles or IoT systems.

Multi-platform delivery. Wallet solutions are typically developed to work across web, iOS, and Android environments. A shared backend is used to keep data synchronized across devices, with APIs feeding multiple front-end applications.

Advanced technology components. Custom builds may incorporate technologies such as machine learning, AI-driven analytics, or blockchain components where required. Examples include fraud detection logic, spending analysis, or user authentication mechanisms designed for specific performance or security needs.

Security-focused architecture. Implementations generally include encryption, secure authentication flows, and adherence to established security guidelines. Depending on requirements, biometric authentication, AI-assisted security checks, or blockchain-based immutability can be incorporated.

Custom analytics and monitoring. Administrative dashboards and reporting tools are usually developed as part of the project. These can include transaction history and monitoring, user behavior analytics, and operational metrics defined by the enterprise.

Why enterprises choose it

Highly specific requirements or differentiation goals. Enterprises pursue custom development when existing platforms cannot support their workflows or when the wallet experience itself is a differentiator. Building from scratch allows full control over features, branding, and interaction models, without adapting to a third-party product's limitations.

Flexible architecture built for long-term needs. Custom projects are often chosen to support specific performance, scale, or regional requirements. When enterprises anticipate complex multi-currency, multi-region, or high-volume scenarios, a bespoke architecture can be designed to match those expectations without compromise.

Deep integration with internal systems. Organizations with legacy infrastructure or proprietary systems often find custom development easier to align with their existing stack. APIs and backend services can be designed specifically to integrate with ERP systems, CRM platforms, internal databases, or even custom hardware.

Ownership of the codebase. Custom development typically results in the enterprise owning the resulting intellectual property or having full rights to modify it. Such a feature appeals to organizations that treat the wallet as core IP or want to avoid ongoing licensing dependencies, even if the upfront investment is higher.

Direct collaboration and ongoing partnership. Working with a development firm provides direct access to engineers and designers throughout the build process. Enterprises sometimes prefer this model when projects involve experimentation or frequent iteration, where close collaboration outweighs the convenience of a ready-made platform.

Limeup (Custom Wallet Development) dashboard.

10. SoftwareGroup (Mobile Wallet Platform)

SoftwareGroup provides an enterprise mobile wallet platform as part of a broader digital banking suite. It's typically used by banks, fintechs, and telecom operators that need to launch large-scale wallet initiatives tied closely to financial services. The wallet solution functions as infrastructure for account-based products rather than a standalone consumer app or loyalty wallet.

Enterprises usually select this platform when the wallet is expected to support regulated financial activity, multi-tenant setups, or national-scale deployments. It's often positioned as a foundation for bank wallets, telco wallets, or ecosystem-style financial applications.

Digital wallet features for enterprises

Account-based wallets and payment capabilities. The platform supports stored-value accounts as well as wallets linked directly to core banking systems. It enables peer-to-peer transfers, merchant payments, integrations with real-time payment schemes, and connections to POS and ATM networks.

Scalable and multi-tenant architecture. The solution is designed to support large user bases and high transaction volumes. It can operate in multi-tenant environments, for example, when a single platform serves multiple banks, brands, or programs.

Omnichannel and agent-based access. In addition to smartphone apps, the wallet can integrate with USSD channels, web portals, and agent banking modules. Features such as bulk disbursements, agent management, and offline operation are commonly used in markets where access to traditional banking is limited.

Broad set of financial services. Beyond payments and transfers, the wallet can support bill payments, QR or NFC merchant payments, savings, loans, insurance integrations, and basic loyalty card storage. Case studies show deployments where payments and loyalty elements coexist within a single application, though financial services remain the primary focus.

Administrative and monitoring tools. Enterprises receive access to management consoles for user administration, fee configuration, transaction monitoring, and compliance controls.

Why enterprises choose it

Established use in financial services environments. The platform has been used in multiple bank and mobile wallet deployments across different regions. Enterprises adopt it as a way to launch bank-grade wallet functionality without building all components internally, particularly when regulatory requirements are high.

Support for varied business models. The wallet can be adapted to different operating models, including bank-led, telco-led, marketplace, or ecosystem approaches.

White-label delivery and customization. The solution is offered as a white-label platform, allowing enterprises to maintain their own branding and UI. Modular components make it possible to enable only selected features and integrate additional services through APIs.

Integration with legacy and national systems. The platform is designed to connect with core banking systems, payment switches, and national infrastructure. Enterprises with complex or older technology stacks often view this as a safer option due to the vendor's experience with similar integrations.

Implementation support and advisory approach. Deployments of large-scale wallets often require guidance beyond software delivery.

SoftwareGroup (Mobile Wallet Platform) dashboard.

11. Mangopay

Mangopay is a modular payment and e-wallet infrastructure provider focused on marketplaces, crowdfunding platforms, and sharing-economy business models. It's designed to support complex money flows where a platform needs to collect funds, hold them securely, and distribute payouts to multiple parties while meeting regulatory requirements. Enterprises typically use it to embed wallet accounts into their platforms rather than to run a standalone consumer wallet.

The solution is commonly adopted by businesses that need escrow functionality, split payments, multi-currency handling, and built-in compliance, without becoming a regulated e-money institution themselves.

Digital wallet features for enterprises

User wallet accounts with escrow support. The platform provides individual wallet accounts for end users, such as buyers, sellers, project creators, or contributors, depending on the business model. Funds can be loaded into these wallets through multiple payment methods, including cards and bank transfers.

Multi-currency handling and international reach. Wallets can hold balances in multiple currencies, which supports cross-border marketplace activity. Enterprises can accept payments in different currencies, maintain separate currency balances, and trigger conversions when needed.

Automated payouts and split payment logic. A core capability is distributing funds programmatically from one wallet to multiple recipients. Enterprises can configure payout rules that automatically allocate funds to sellers, service providers, platform accounts, or third parties.

Built-in compliance workflows. Identity verification and transaction monitoring are integrated into the wallet lifecycle. KYC checks are triggered when regulatory thresholds are reached, and AML monitoring runs continuously.

API-driven and modular architecture. The platform exposes well-documented APIs that allow enterprises to adopt specific components as needed. Some organizations use it primarily for payment acceptance and payouts, while others rely on the full wallet, escrow, and compliance stack.

Why enterprises choose it

Purpose-built for platform and marketplace models. Enterprises running two-sided or multi-party platforms select this solution because it addresses escrow, fund holding, and split payments as first-class features.

Faster route to compliant payment operations. Integrating with a regulated provider allows enterprises to launch payment and wallet functionality without securing their own e-money licenses (it shortens time to market and simplifies expansion across regions, particularly in Europe, where regulatory requirements are strict).

Improved trust for end users. Escrow functionality and regulated fund handling help platforms build credibility with buyers, sellers, and contributors. Users are reassured that funds are held securely and released according to defined rules, which is particularly relevant for crowdfunding, peer-to-peer marketplaces, and service platforms.

White-label experience with backend abstraction. Payment and wallet operations run behind the scenes under the enterprise's brand. Users interact only with the platform's interface, while Mangopay handles fund movement, compliance checks, and payout execution.

Scalability and operational support. The infrastructure is designed to scale as transaction volumes and user counts grow. Enterprises also reference onboarding support, sandbox environments, and guidance around verification flows and payout optimization as factors when choosing the platform.

Mangopay dashboard.

Why Open Loyalty's Wallet Software Stands Out

Looking across the market, most digital wallet solutions stop at transactions, passes, or balances. Open Loyalty takes a different path by treating wallets as an active part of loyalty and customer engagement, not a standalone utility.

The sections below break down what sets this approach apart when wallets need to support real programs, real customers, and long-term growth at enterprise scale.

Open Loyalty treats wallets as a natural extension of loyalty programs, not a separate layer that needs stitching in later. Points, rewards, cashback, and offers live directly inside the wallet logic, so what customers earn and use stays in one shared balance experience.

Enterprise teams can run multiple balance types side by side, such as monetary funds, loyalty points, or short-term promotional credits, each following its own rules.

Spending can unlock rewards instantly, and those rewards appear in the wallet straight away. That opens the door to flows like earning points during checkout and using them moments later, or combining long-term points with time-limited offers without extra work behind the scenes.

Many wallet solutions start with transactions and treat loyalty as something to connect later. In practice, that often means syncing data across systems and handling edge cases manually. Open Loyalty flips that order.

Wallets come with built-in support for points, tiers, rewards, and promotions, which lets enterprises design programs where transactions and loyalty activity move together, instead of circling each other from separate systems.

Open Loyalty is built around open APIs and webhooks, with every wallet function available programmatically. The platform runs fully headless, which gives enterprise teams freedom to plug wallet logic into any touchpoint they already run, from mobile apps and websites to in-store POS systems or connected devices.

Developers decide where and how wallet features appear. A points balance can show up inside an account screen, a reward can surface during checkout, and a QR code from the wallet can be scanned at the counter, all using the same backend logic. No locked SDKs, no forced UI patterns, and no need to bend existing systems to fit the wallet.

That flexibility makes a real difference in complex environments. Enterprises often operate across multiple channels and regions, each with slightly different requirements. A headless setup lets teams reuse the same wallet rules everywhere, while tailoring the front-end experience to each channel without hacks or parallel implementations.

Open Loyalty lets enterprises run several wallets at the same time for a single customer. Points, cashback, gift card balances, or promotional credits can all live side by side, each with its own logic and lifecycle.

Each wallet can follow different rules. One balance might expire after 90 days, another might roll over indefinitely, while a third is tied to a specific campaign or region. All of this is handled within one customer profile, without splitting data across systems or creating special cases in the frontend.

This setup works well for programs that go beyond a single points balance. Enterprises can separate long-term status tracking from short-term incentives, test new reward mechanics without touching core balances, or support multiple regions with different reward structures. Everything stays organized, predictable, and easy to reason about, even as programs grow in complexity.

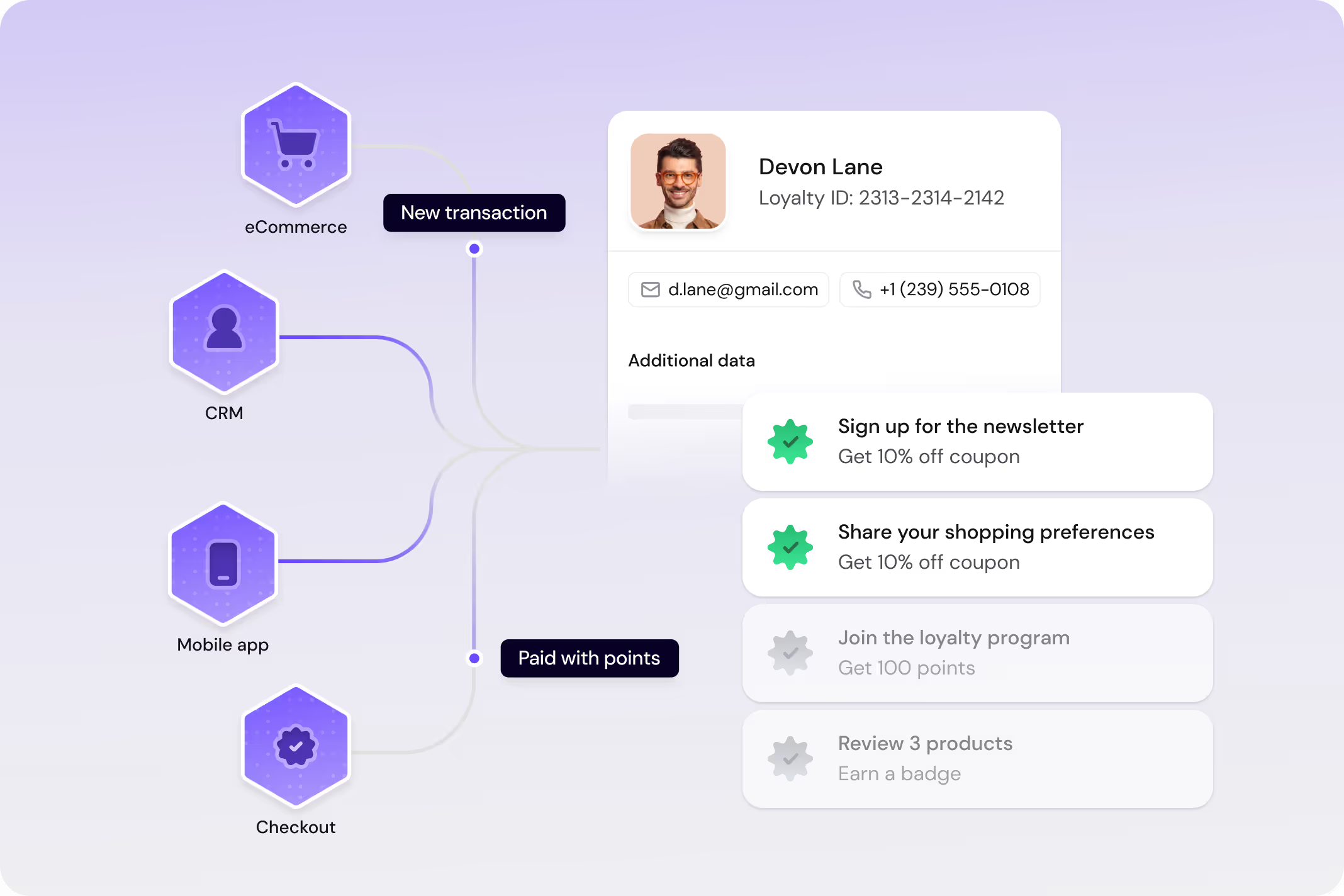

Open Loyalty brings wallet activity from every channel into one shared picture. In-store purchases, online orders, and mobile app actions all feed into the same balances and update in real time.

Customers always see the current state of their wallet. Points earned at the counter show up straight away in the app, and those points can be used online moments later. No waiting, no manual refresh, no guessing which balance applies where.

For enterprise teams, this removes channel boundaries at the data level. Wallet rules apply consistently across touchpoints, so there's no need to maintain separate balances for online and in-store activity. Programs stay easier to manage, and customers get a smoother experience that feels coherent wherever they interact.

Omnichannel in Open Loyalty. Source: https://www.openloyalty.io/product/customer-gamification-software

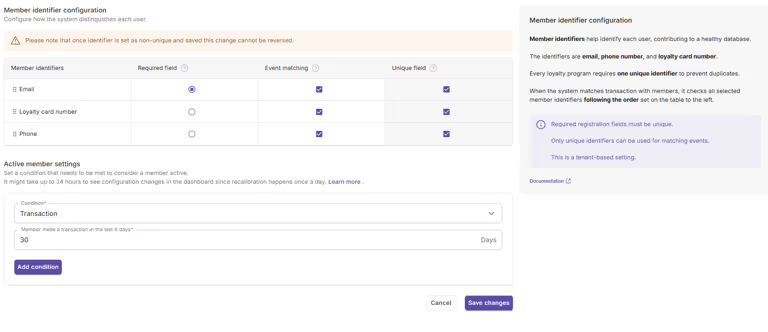

Enterprise scalability and security

Open Loyalty's wallet engine is built for large deployments. Programs can handle hundreds of millions of API calls per month while keeping response times comfortably low, even during peak traffic. That matters when wallets need to update balances in real time for millions of members across multiple channels.

Deployment options cover both cloud and on-premise setups, so enterprise IT teams can match internal policies, data residency requirements, and existing architecture instead of reshaping everything around a single hosting model.

Security and compliance are treated as baseline requirements. The platform is ISO 27001 certified and supports GDPR compliance, which helps enterprises meet internal security expectations and regulatory obligations while running loyalty wallets at scale.

Security in Open Loyalty. Source: https://www.openloyalty.io/news/open-loyalty-iso-certifications

Rich configuration (no coding needed)

A large part of wallet setup and ongoing changes can be handled directly from the admin interface. Marketing and loyalty teams can configure earning and spending rules, adjust expiration logic, or launch bonus campaigns without pulling developers into every change.

That setup supports faster iteration in day-to-day program work. A limited-time "double points" promotion can be rolled out from the dashboard and applied across all wallets straight away, without releases, workarounds, or waiting on development cycles.

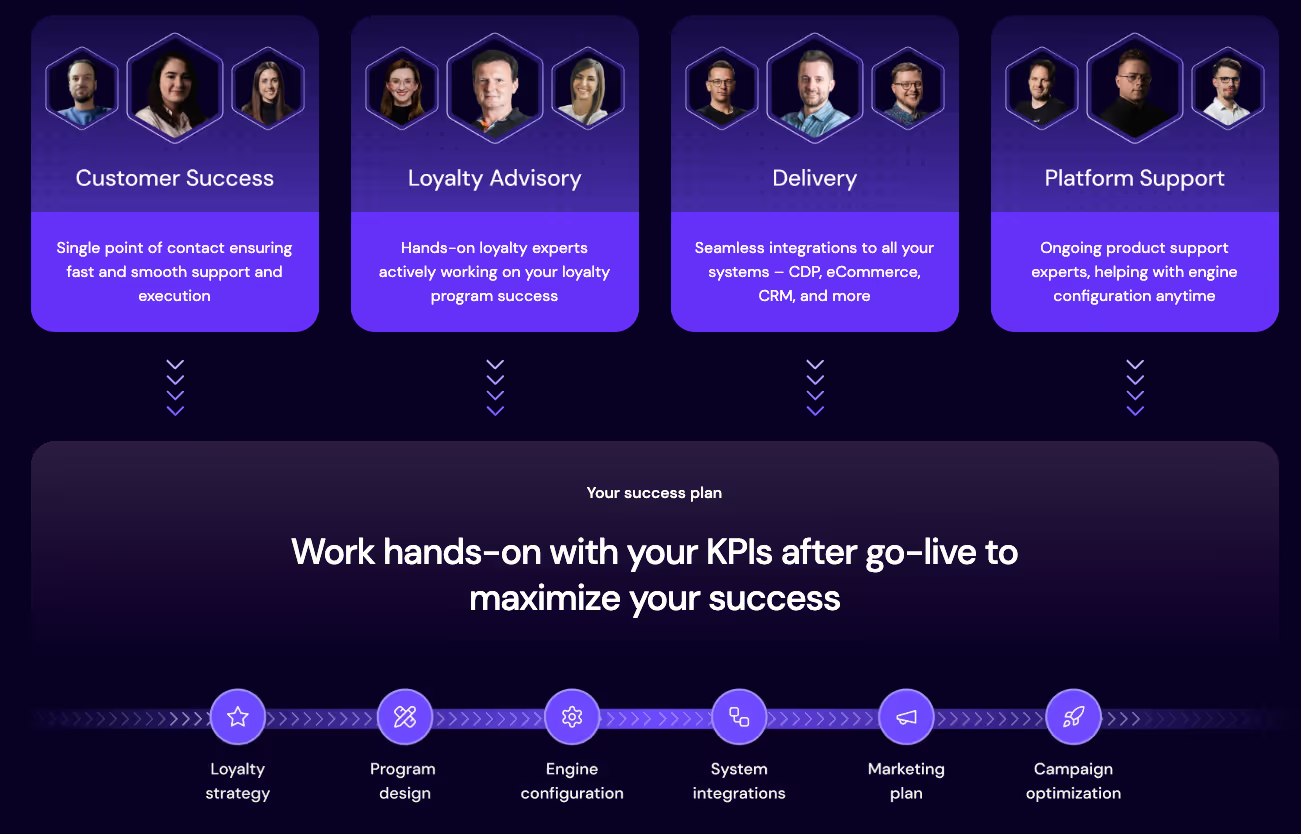

Open Loyalty comes with access to people who work with loyalty programs every day, not only with software. Enterprise teams get support that goes beyond technical setup and into program design, rollout planning, and day-to-day optimization.

The team shares practical guidance based on real implementations across industries, including what tends to work, where teams usually get stuck, and how programs evolve over time. That support often includes ready-to-use resources such as implementation checklists or industry trend insights, which help teams make better decisions without starting from scratch.

Alongside that, there's an active group of developers and practitioners building on the platform. The shared knowledge base makes it easier to solve edge cases, exchange ideas, and move faster when programs grow in scope or complexity.

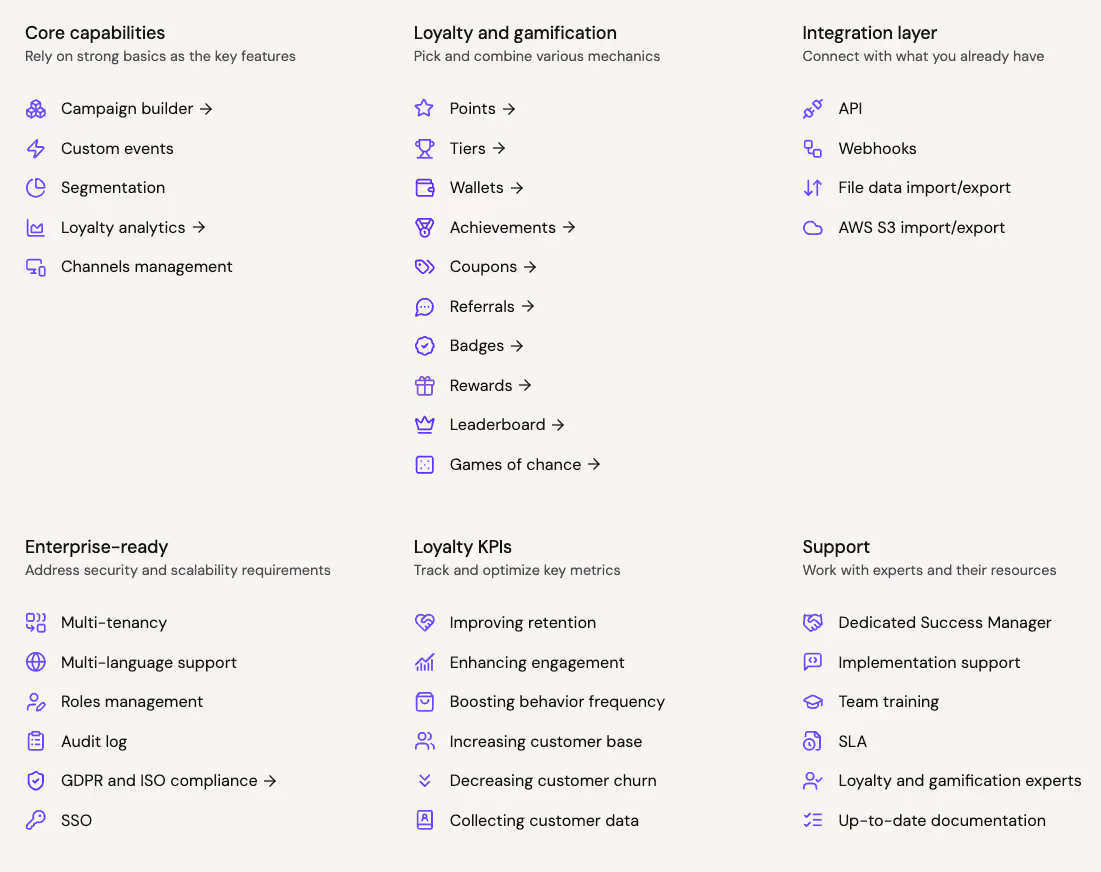

The wallet in Open Loyalty sits inside a broader loyalty stack rather than operating on its own. Campaign management, analytics, gamification mechanics, and other loyalty components connect directly to the same wallet logic and customer data.

That setup gives enterprise teams room to grow over time. A program can start with wallets and balances, then later introduce tiers, challenges, referrals, or new reward mechanics without reworking the foundation. Everything plugs into the same structure and stays aligned with existing wallet rules.

Enterprises often look for a path that does not lock them into a single use case on day one. Having wallets as part of a wider ecosystem makes it easier to evolve programs gradually, without stitching together multiple tools or migrating data as ambitions expand.

Simply, yes. Enterprises can create their own digital wallet, but there are different paths to consider. Some teams build a wallet from scratch, which offers full control over features and branding but comes with longer timelines and ongoing responsibility for security, scaling, and maintenance.

Others use dedicated wallet software that provides wallet infrastructure, APIs, and admin tools, allowing teams to focus on program logic and customer experience rather than low-level wallet mechanics.

What are the three types of digital wallets?

From an enterprise perspective, digital wallets generally fall into three categories:

Ecosystem wallets, such as Apple Wallet or Google Wallet, which act as customer-facing storage for cards and passes

Checkout or payment wallets, designed to speed up online and mobile payments

Enterprise wallet platforms, which manage balances, rules, and logic for rewards, stored value, or complex programs

Most enterprise setups combine more than one type, using ecosystem wallets on the front end and a platform behind the scenes.

How do I set up a digital wallet on my phone?

Most smartphones come with a built-in digital wallet app.

On iPhones, the wallet is preinstalled and can be accessed directly from the device.

On Android phones, a wallet app is also included or can be enabled through system settings. Users usually add payment cards or loyalty cards by scanning them or confirming details inside the app.

From an enterprise perspective, customers typically add wallets through links, QR codes, or in-app prompts provided by the business rather than setting everything up manually.

What is a rewards wallet?

A rewards wallet is a digital wallet that stores non-monetary balances such as loyalty points, cashback, vouchers, or promotional credits. In enterprise setups, rewards wallets are connected to loyalty rules, campaigns, and customer profiles, allowing customers to earn and redeem rewards across channels in real time.

What is a loyalty wallet?

A loyalty wallet is a digital wallet designed specifically to manage loyalty-related balances. It typically holds loyalty point balances, tier status, rewards, and digital loyalty cards. Enterprises use loyalty wallets to keep rewards visible, accessible, and usable at the moment of purchase.

What are wallet points?

Wallet points are loyalty points stored inside a digital wallet rather than a standalone loyalty database. They update automatically after purchases or actions and can be redeemed online, in-store, or in-app, depending on program rules.

How much are 5,000 loyalty points worth?

The monetary worth of 5,000 points depends entirely on the program's conversion logic. Some enterprises set a fixed rate (for example, 100 points = €1), while others use dynamic pricing or reward catalogs. Wallet software allows enterprises to control these rules centrally.

Can you store loyalty cards in a digital wallet?

Yes. Many digital wallets allow customers to store digital copies of loyalty cards. These cards can display point balances, barcodes, or QR codes and often support lock screen notifications when customers are near favorite stores.

Does Apple Wallet allow loyalty cards?

Yes. Apple Wallet supports loyalty cards, membership cards, and reward passes. Enterprises typically use APIs or pass platforms to issue cards that customers can add to their Wallet and access quickly from their phone.

What is a Google Wallet loyalty card?

A Google Wallet loyalty card is a digital version of a brand's loyalty card stored in the Google Wallet app. It can display point balances, member details, and barcodes, and it can trigger lock screen notifications based on time or location.

Is there one app for all loyalty cards?

Consumer wallets like Apple Wallet and Google Wallet can store multiple loyalty cards in one place. From an enterprise perspective, a loyalty wallet platform sits behind these apps, managing balances, rules, and reward logic across all stored cards.

What is a reward wallet used for in enterprises?

Enterprises use reward wallets to:

Store loyalty points and promotional credits

Allow customers to redeem rewards instantly

Connect rewards with payments and transactions

Keep loyalty data consistent across channels

Reward wallets are often tied to CRM and analytics systems for deeper insights.

What is loyalty point balance?

A loyalty point balance shows how many points a customer has available at a given moment. In wallet-based programs, this balance updates in real time and can be displayed across apps, websites, POS systems, and digital wallets.

What is an open wallet?

An open wallet is a wallet system built on APIs that can integrate with multiple channels, payment providers, and front-end experiences. Enterprises use open wallets to avoid being locked into a single ecosystem while keeping control over customer data and financial info.

What are the main types of digital wallets?

From an enterprise perspective, digital wallets usually fall into three categories:

Ecosystem wallets (for example, Apple Wallet or Google Wallet)

Checkout wallets focused on faster payments

Enterprise wallet platforms that manage balances, rewards, and rules

Each type solves different problems and often works together in one setup.

How do customers redeem rewards from a digital wallet?

Customers typically redeem rewards directly during checkout, by scanning a wallet barcode in-store, or by selecting rewards inside an app. Enterprise wallet software controls redemption rules, availability, and balance updates in real time.

Do digital wallets store financial information?

Some wallets store financial transactions info such as payment tokens or stored balances, while others focus only on rewards or passes. Enterprise platforms usually separate payment data from loyalty data and rely on integrations for secure handling.

Are digital wallets relevant for small businesses?

Yes, but the setup differs. Small businesses often rely on consumer wallets or lightweight loyalty tools, while enterprises use wallet software that supports scale, multiple locations, advanced rules, and analytics.

What do Gen Z use instead of physical wallets?

Gen Z users rely heavily on mobile wallet app solutions. They store payment methods, loyalty cards, digital copies of tickets, and even IDs such as a driver's license where supported. The spotted behavior makes wallet-based loyalty programs more visible and easier to use.

Most modern smartphones come with a built-in digital wallet app:

iPhones include Apple Wallet

Android devices include Google Wallet

Enterprises design wallet experiences assuming these apps are already present on customer devices.

Choose the digital wallet that aligns with your enterprise needs

Across all the solutions covered in this guide, one thing becomes clear: digital wallets solve very different problems depending on how they are built and where they sit in the stack. Some focus on payments, others on passes or checkout speed.

Digital wallets are getting stronger and account for ~49% of global eCommerce transaction value. Wallets have surpassed credit cards as the most commonly used online payment method worldwide.

Open Loyalty takes a broader, more connected approach as its wallet software brings transactions, rewards, and customer engagement into one flexible platform. Wallet balances are tightly linked with loyalty logic, campaign rules, and real-time activity across channels. That setup fits enterprises that treat loyalty, payments, and engagement as parts of the same system rather than separate initiatives.

For teams looking to launch a wallet that goes beyond storage and supports long-term customer relationships, Open Loyalty offers a clear path. Programs can start simple and grow over time, adding new mechanics and experiences without rebuilding the foundation. The result is a wallet that supports everyday transactions while helping enterprises strengthen retention, increase repeat usage, and build loyalty that lasts.

Weronika is a Content Manager with over four years of experience in loyalty and gamification. She has a deep passion for telling stories to educate and engage her audience. In her free time, she goes mountain hiking, practices yoga, and reads books related to guerrilla marketing, branding, and sociology.

Join the community of 4,000 Loyalty Builders!

Get a weekly dose of actionable tips on how to build and grow gamified successful loyalty programs!

Customer loyalty know-how

Leverage resources from Open Loyalty’s gamification and loyalty experts to start smooth and move in the right direction